After the SVB blowup and banking crisis that followed, the talk was what will be the next shoe to drop. Where does the contagion spread to? I started to hear a lot of rumblings about commercial real estate (CRE). Then some stories started to get written on it. To me it seemed like dot connecting but nothing in the data yet supported it. Then we started to see some charts and data roll out.

Last week I started to really pay attention and do some more research after seeing this from Lisa Shalett CIO, Wealth Management at Morgan Stanley. She wrote the following in a note last week.

Commercial real estate (CRE): Investors have sharpened their focus on this sector, given regional banks’ significant share in CRE lending. Even before the banking-industry turmoil, however, CRE was facing risks from long-term trends, with remote work threatening the office sub-sector.

What’s more, the sector is now facing a huge “refinancing wall”: More than half of the $2.9 trillion in commercial mortgages will be up for refinancing in the next couple of years. Even if current rates stay where they are, new lending rates are likely to be 3.5 to 4.5 percentage points higher than they are for many of CRE’s existing mortgages.

Commercial property prices have already turned down, and Morgan Stanley analysts forecast prices could fall as much as 40%, rivaling the decline during the 2008 financial crisis. These kinds of challenges can hurt not only the real estate industry, but also entire business communities related to it.

That will definitely catch your attention and raise your curiosity. The first part I wondered was just how much of a share does the already embattled small and medium-sized banks have in CRE lending exposure?

It turned out much higher than I expected. Then for the overall share of all commercial mortgage holders by firm type (excluding multifamily) is heavily banks. The exposure does also spill into a couple other categories.

On top of banks losing deposits, dealing with higher interest rates and tighter lending standards, this is another worry they’re going to have hanging over them.

Does the CRE part of this really seem to cause a reason for concern though? We already know how the pandemic increased the move to an increasing number of employees working from home. All those people worked within a CRE structure somewhere prior. Companies are then able to downsize in square footage or let their leases expire as they come due.

I had thought that since the pandemic is now in the rearview mirror and it will have been over three years since it began, that the CRE usage and vacancies would have normalized and leveled off. Not quite the case.

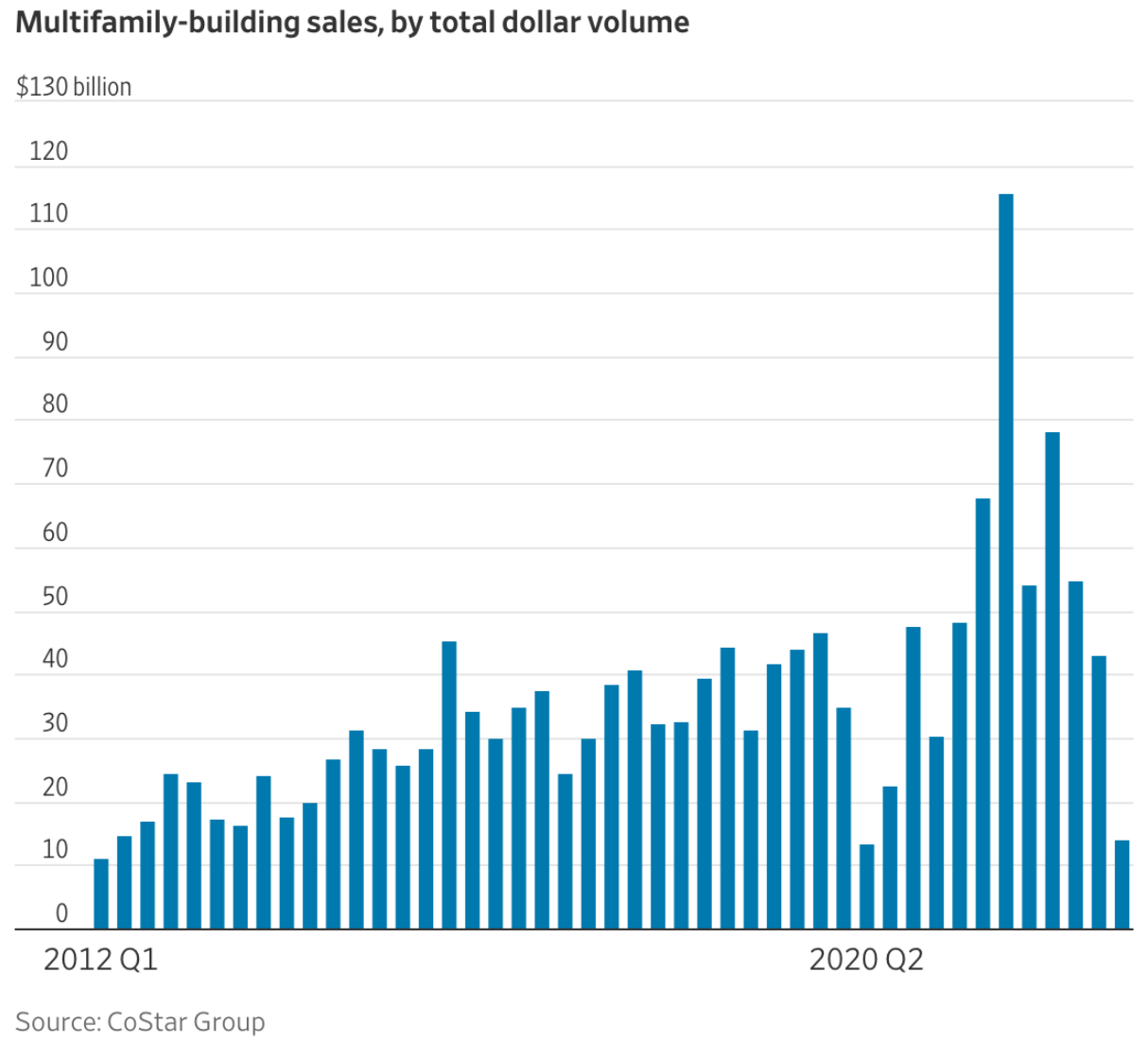

While vacancies are rising. Multifamily-building sales are also way down.

What isn’t helping an immediate bounce back is that bank lending has fallen overall in both commercial and personal related loans. This was a survey done by Apollo of 71 banks within the Dallas Fed district. A credit and lending crunch looks to have already started.

Here’s a two week change chart in commercial real estate loans from US Banks.

We’ve seen how fast the Fed has raised rates. It’s having a direct impact. They’ve gone too far too fast. They say they’re data dependent but the data is on a lag. There hasn’t been enough time to see the full impact of these rate hikes. It has to work through the system. Tightened lending doesn’t help business expansion or hiring. It affects business owner sentiment and now reflects that in the NFIB Small Business Hiring Index, which has tumbled in March.

NFIB Small Business Good Time to Expand results hit a 43-year low. It’s now at the same levels as March 2009. The only time it was lower was in 1980.

Banks are losing deposits and not lending. Loan availability for small businesses is at the worst levels in a decade.

You’ve essentially taken away a vital business partner to small and medium sized businesses. They rely on banks to partner with them to expand, hire, invest in new equipment and have access to working capital. Wall Street doesn’t fund this growth, banks do.

What fills CRE is businesses. As businesses expand and need more room, they fill the CRE spaces. That demand and outlook has weakened, therefore the vacancies are increasing and sales are non-existent. Lending standards and high interest rates provide no help. As vacancies rise, no buyers present, companies not expecting to hire or expand is where the formula doesn’t paint a very bright outlook.

If the Fed pauses the hiking of rates and starts to cut like the below chart of Fed Funds Futures predicts, some relief may come. They almost seem like they’ll have to. With all that’s connected there is a reasonable concern for the economic health ahead. We just have to hope that too much damage isn’t already done.

If you’d like to read more about this, there were the following stories recently written.

A $1.5 Trillion Wall of Debt is Looming for US Commercial Properties via Bloomberg

Office Vacancies Send Real-Estate Investors to the Exits via WSJ

Commercial Property Debt Creates More Worries via WSJ

The coming commercial real estate crash that may never happen via CNBC

The Coffee Table ☕

I just finished reading The Creative Act: A Way of Being by Rick Rubin. I’ve had this book recommended to me by two Spilled Coffee subscribers so I was very curious about it. Turns out they were right. This is one of the best books that I’ve read. Rick Rubin’s past speaks volumes but his writing just hits the nail on the head. Very well done. A timeless type of a book that I plan to read again.

One of my favorite TV shows is back! Succession Season 4. This is the final season of the show and it’s off to an excellent start. The acting in this show is superb. You can see why it wins as many awards as it does. I’ll miss this show once it completes.

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe and/or give a gift subscription for others.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.