Is Housing Next To Fall?

Examining the health of the housing market

We continue to see the economy and financial assets whipsaw in all directions. Currently that direction seems to be downward for financial assets. The stock market is in a bear market. Companies that saw large spikes from the pandemic have seen their stock prices fall to where they were or even lower prior to the pandemic. It’s like the pandemic surge they received, never happened. Bonds are having one of their worst years ever. Crypto has seen a massive selloff as Bitcoin is down about 60%.

Assets that rocketed upward have taken the elevator back down. The riskier the assets, the bigger the drop they’ve experienced. We’re witnessing a rerating of financial assets.

But what about housing? One of the hottest sectors over the past two years has yet to join the sell-off party. Is it just arriving late? Or is it going to be able to hold off and buck the selloff trend?

Rising Costs

Homeownership in the U.S. is at 65%. Homes are the most widely held asset in this country. This is why the trajectory of what housing does is so important to so many.

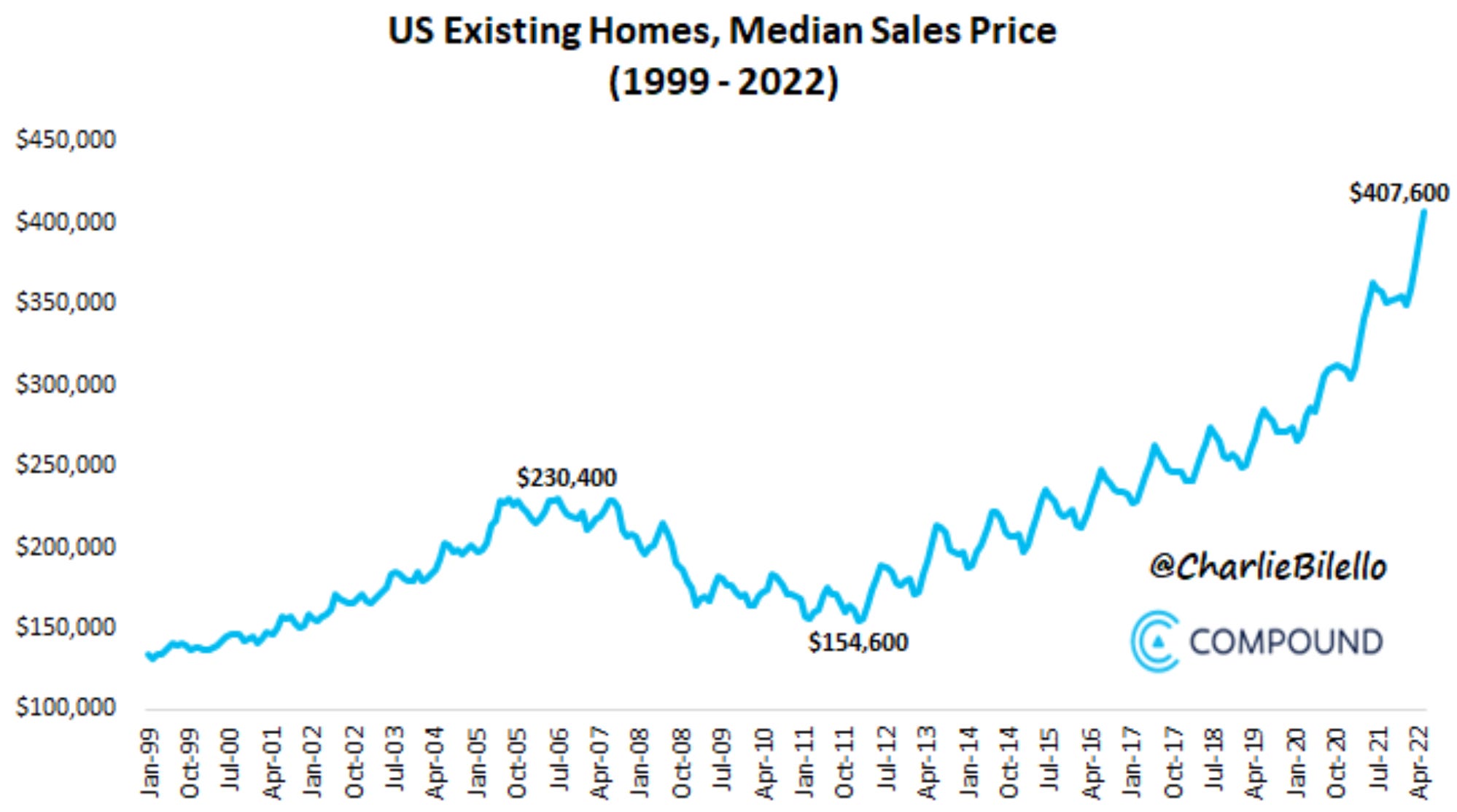

We’ve all seen what housing prices have done. You or someone you know has a story about getting so much more than they thought for their house or there were this many offers above the asking price on their home the first day. The wild west in housing has pushed the median sales price of a home to an all-time high of $407,600.

This run up in housing isn’t alone. The national average cost for rent has also touched a new all-time high of $1,362 a month.

U.S. consumers have seen a drastic increase in the cost of shelter, whether owning or renting. With rent rising right along with the cost of owning a home, you can’t blame renters for wanting to become homeowners.

The remote work and job availability boom has opened up where people can now live and work. If you’re paying high rent in a big city and can’t afford a home in that area, many have picked up and moved to an area where they can purchase a home. Remote work is allowing for many more options than in the past.

Rates Have Jumped

With housing costs in the midst of a white hot period we’re now seeing the Fed intentionally trying to cool it off. Mortgage rates have gone from 3% to pushing over 6% of late.

How much of an impact does a mortgage increase from 3% to over 6% make to borrowers? Ben Carlson put together a chart comparing a 3% mortgage rate versus a 6.3% rate. As you can see, the monthly payment on a $400,000 home, increased by over $700 per month.

Payments are obviously much higher at 6.3% than 3%, but they aren’t unaffordable. We’re just used to a very low interest rate environment. Many lived through the era with interest rates in the 12%+ range and homes still sold. Homes will continue to sell at the higher mortgage rates. It’s understandable that demand will cool a bit with higher rates, but it has to. The overwhelming demand and wild west that housing was experiencing isn’t healthy and needs to stabilize by finding a new normal level.

Is It 2008 Again?

When you bring up the thought of a housing downturn, you can’t have that discussion without right away someone jumping in to say, “here comes 2008 again.” I heard it multiple times over the holiday weekend. The same people who blurt that out, also have a comment about the stock market as well “Here comes the next dot com crash.” Those are the people who I all of a sudden get the urge to use the excuse that I need to head to the bathroom just to get away from them. I’ll let them cast their negativity about everything, onto someone else.

The data points to U.S. home owners being in the best shape they’ve ever been in. They’re seeing all-time high home equity levels in their homes.

Mortgage debt payments as a percentage of disposable personal income is sitting at record lows of under 4% in Q1.

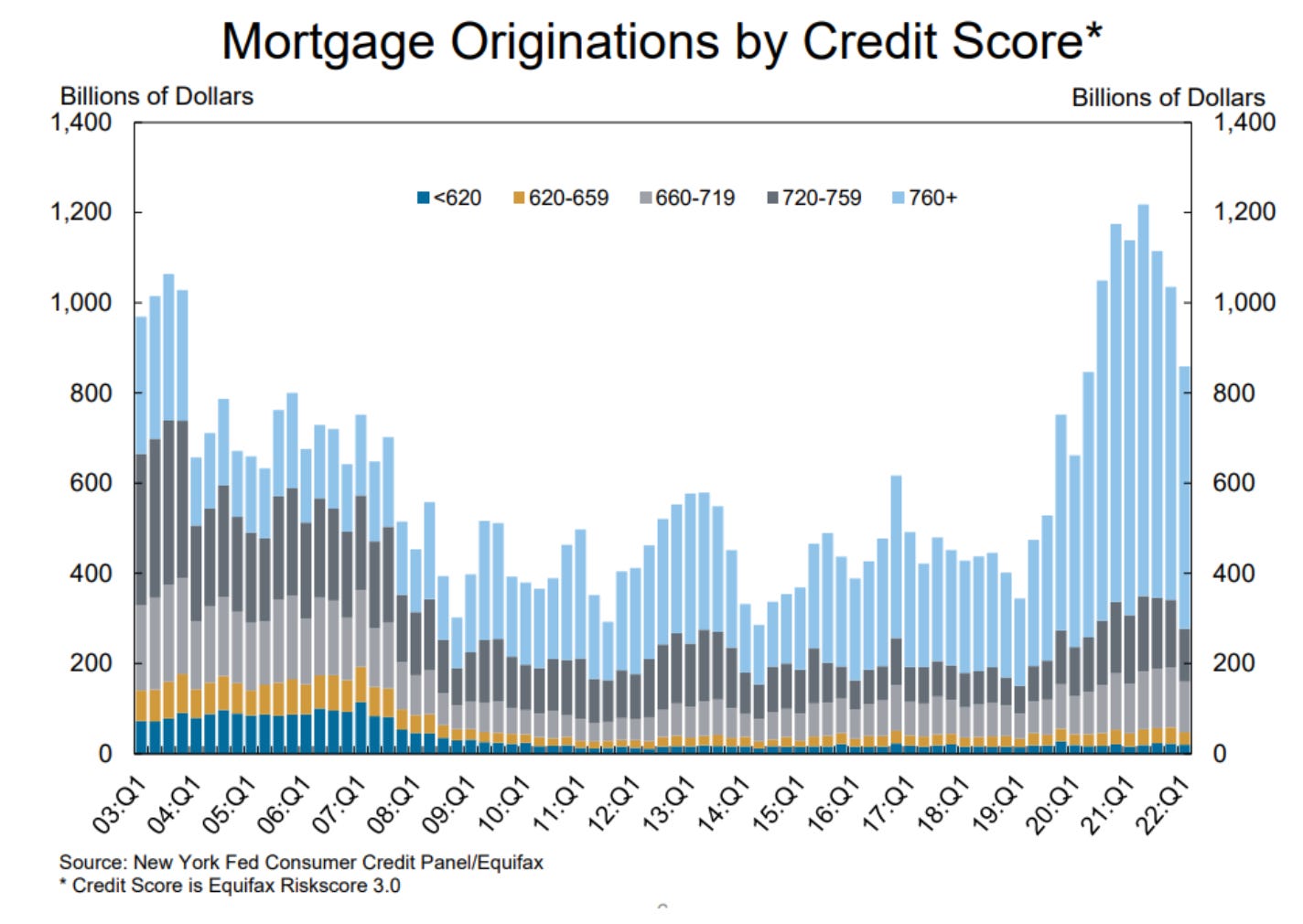

I’ve also heard the pushback that with all these home sales, surely the banks are getting people into homes they can’t afford and the lending standards must have relaxed like the timeframe leading up to the 2008 GFC. Actually the opposite has occurred.

Data shows that the mortgage originations by credit score has improved dramatically. Look at the credit quality of the mortgages these past few years.

The underlying foundation to the current housing boom does look rather solid. It's been a closely watched and dissected sector of late. There just haven’t been any glaring warnings signs. Maybe this domino doesn’t fall like the other financial assets?

You can’t panic sell your house like you can a stock, mutual fund, ETF or cryptocurrency. It’s not something as liquid as the other financial assets where it can be sold with a click and completed in seconds. Housing is viewed as a safe asset. It’s the ultimate long-term investment.

Jobs Provide the Fuel

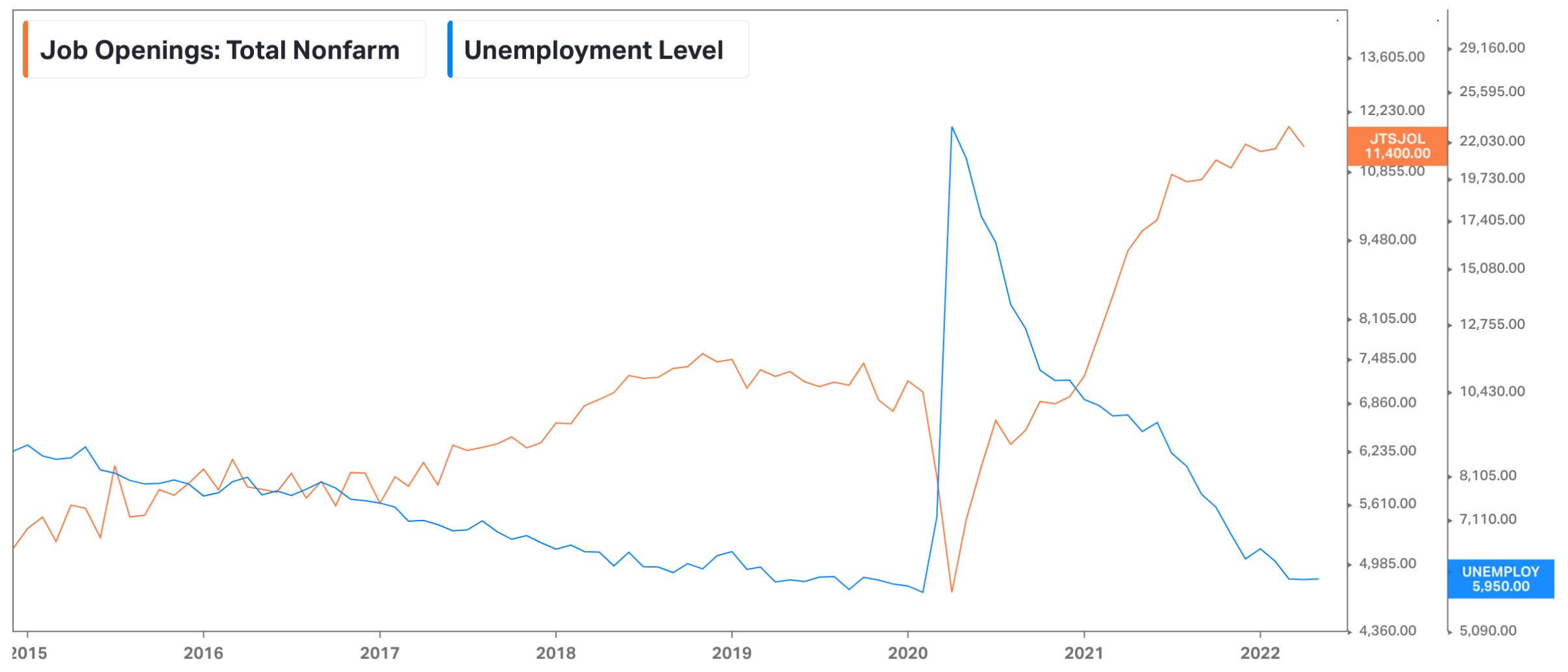

If there is one data point that needs to be watched very closely in my view, it’s the jobs picture. The job market has seen the best period for consumers in decades.

There are almost two jobs available for every one unemployed person. With the job market this strong it helps with the economics of housing. People are employed and able to trade up for better paying jobs. With the ability to work remotely it expands where someone can buy a home and live regardless where their company is based. I believe that the robust job market has been one of the biggest reasons we’ve seen what we have in housing. If it continues to be strong, housing will continue to be strong.

What Tells the Story?

Is there a certain data point that we can monitor to see if housing starts to shift? How will we know if things are starting to change?

Watch the inventory levels. This will be the major data point to monitor. It will tell the story of housing.

As inventory remains low, there are fewer options to buy, therefore pushing pricing up. Demand has far and away exceeded the supply the past two years. If inventories start to climb, that will put pressure on pricing. It will naturally cause prices to fall.

Everything mentioned above comes together to form what inventories ultimately do. Think of it as a recipe. Right now the recipe is creating a good outcome for U.S. consumers. Let’s hope that continues.

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe and/or give a gift subscription for others.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.