Investing Update: Q1 Recap & Q2 Outlook

What I'm buying, selling & watching

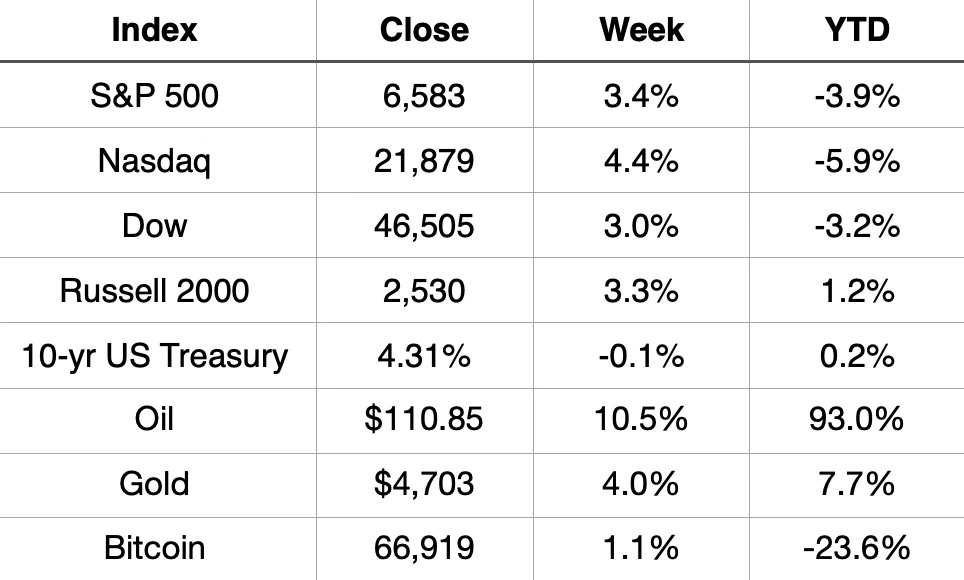

The S&P 500 snapped a five-week losing streak, gaining 3.4% to close at 6,583. The Nasdaq led the bounce at +4.4%. The Dow added 3.0%. All three are still underwater for the year, but this was the first week since the Iran war began where buyers showed up with conviction.

Oil tells the real story of the week. WTI surged 10.5% to close at $110.85 a barrel, and briefly touched $115 before the Hormuz headlines cooled it off. Oil is now up 93% for the year. That number is not a typo.

Gold had a strong week too, up 4.0% to $4,703, and is now up 7.7% on the year. The 10-year Treasury yield ticked down slightly to 4.31%, a sign that bond markets are at least not panicking further for now.

The Russell 2000 remains the only major index in positive territory for 2026, up 1.2% YTD. Small caps are less exposed to the global earnings pressure that high oil creates for multinationals. Worth watching.

Bitcoin is still stuck. Up 1.1% on the week, but down 23.6% for the year. Risk-off has not been kind to crypto.

One week does not make a trend. But after five straight weeks of selling, the bulls finally had something to cheer about.

Market Recap

Weekly Heat Map Of Stocks

YTD Heat Map of Stocks

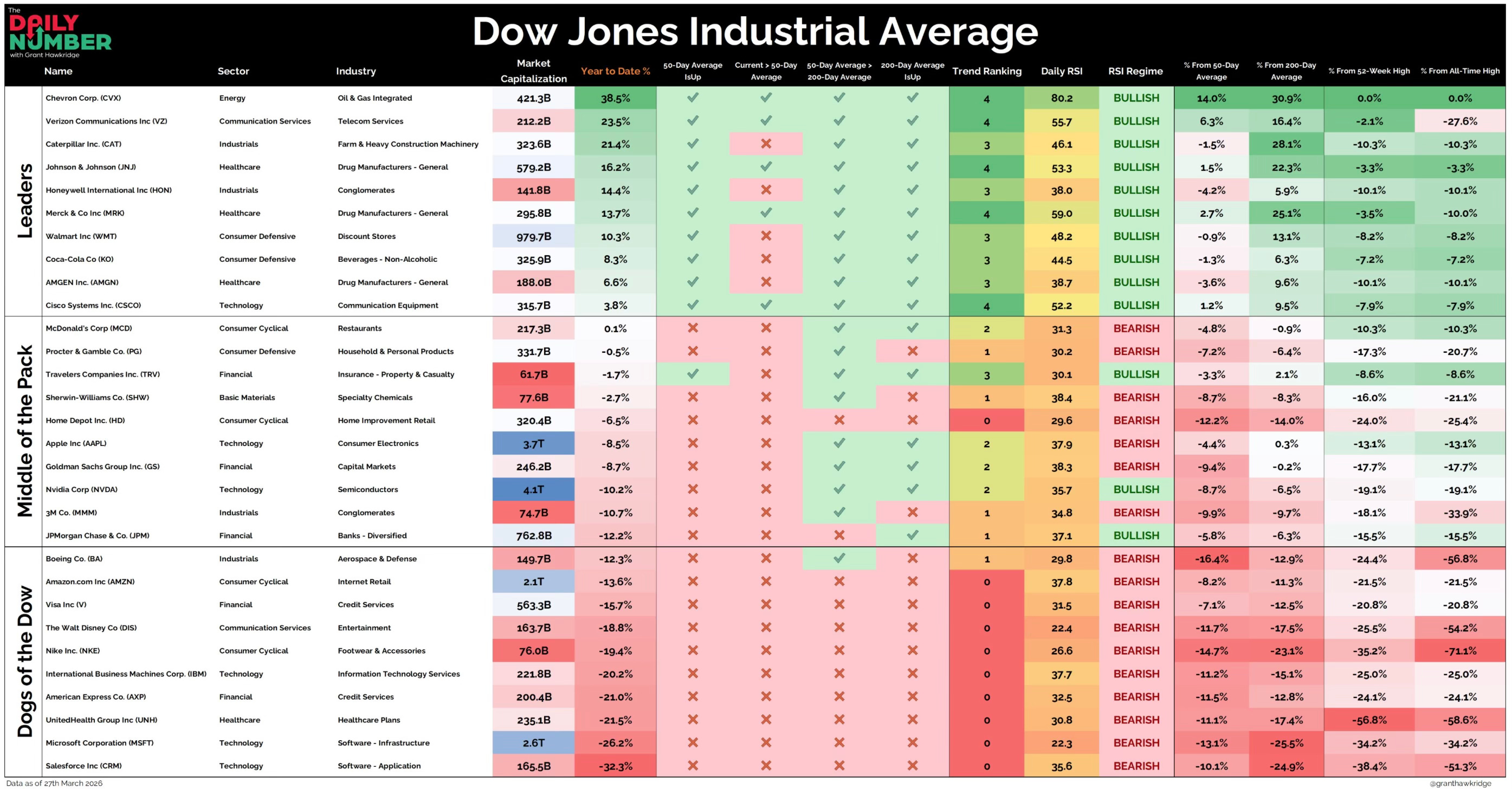

The Dow Report Card

Q1 Recap

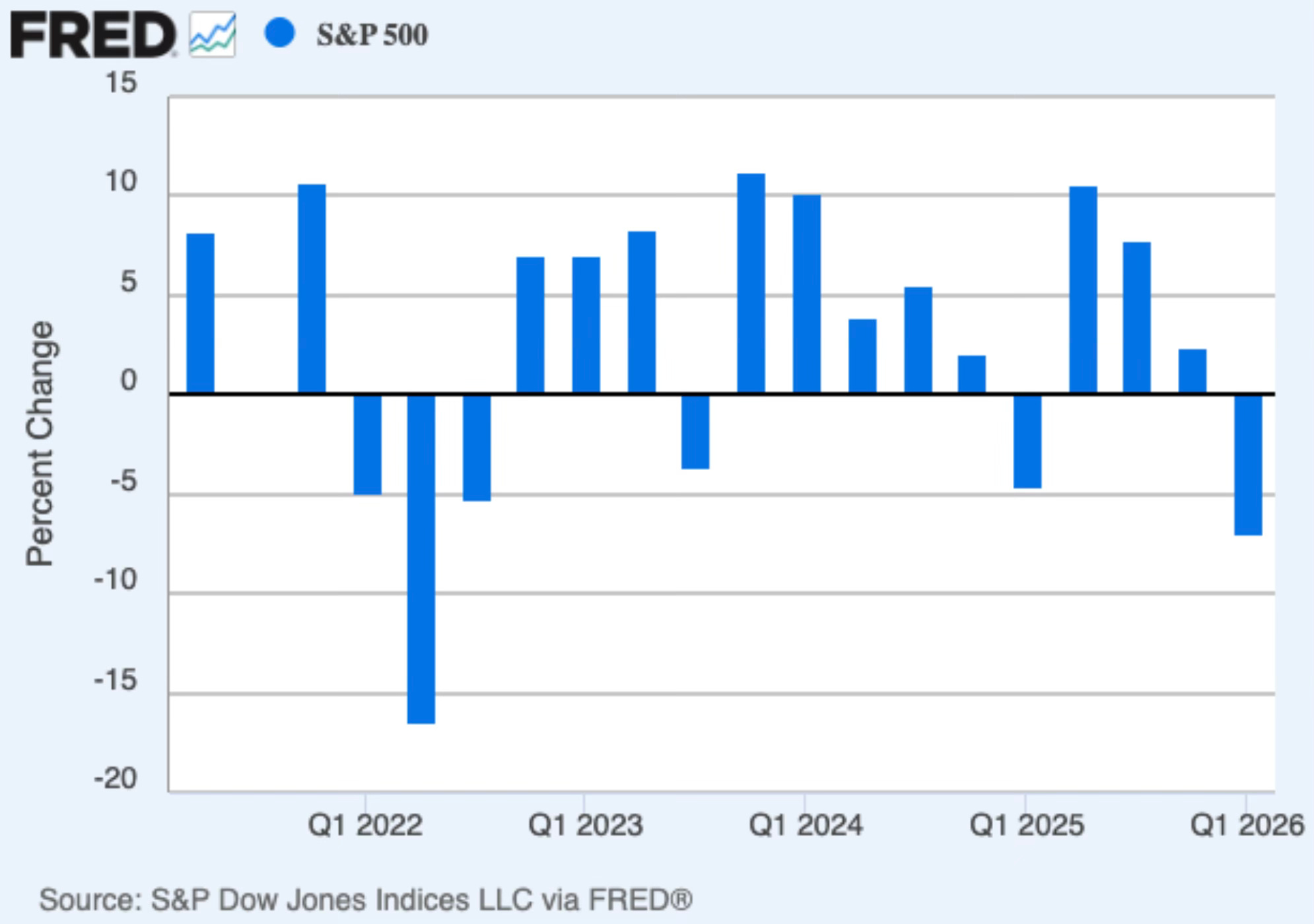

The first quarter is in the books. It wasn’t pretty.

The S&P 500 finished Q1 down 4.6%. That’s the worst quarterly performance since Q3 2022, when Russia’s invasion of Ukraine rattled global markets. Three years of double-digit gains, gone in 90 days.

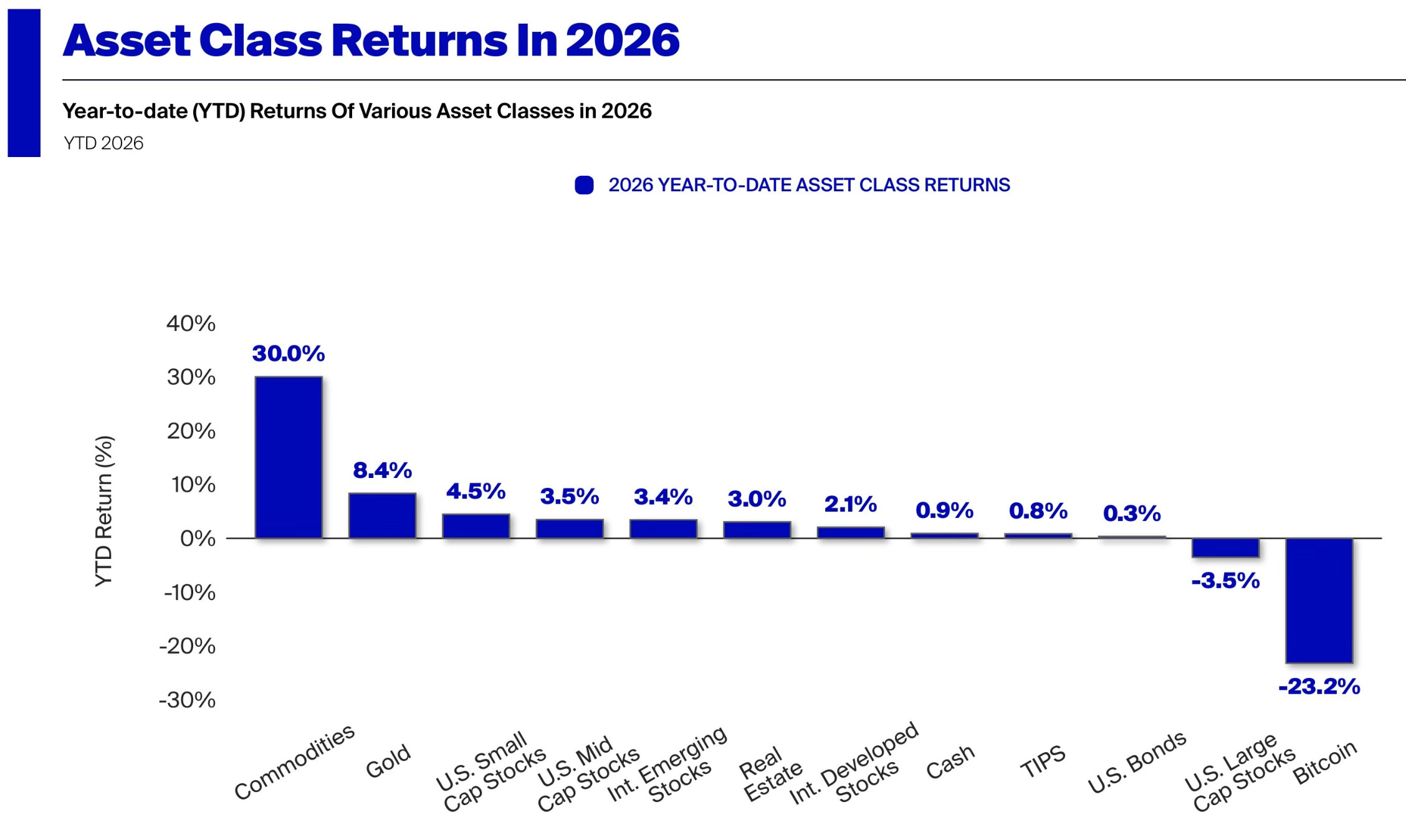

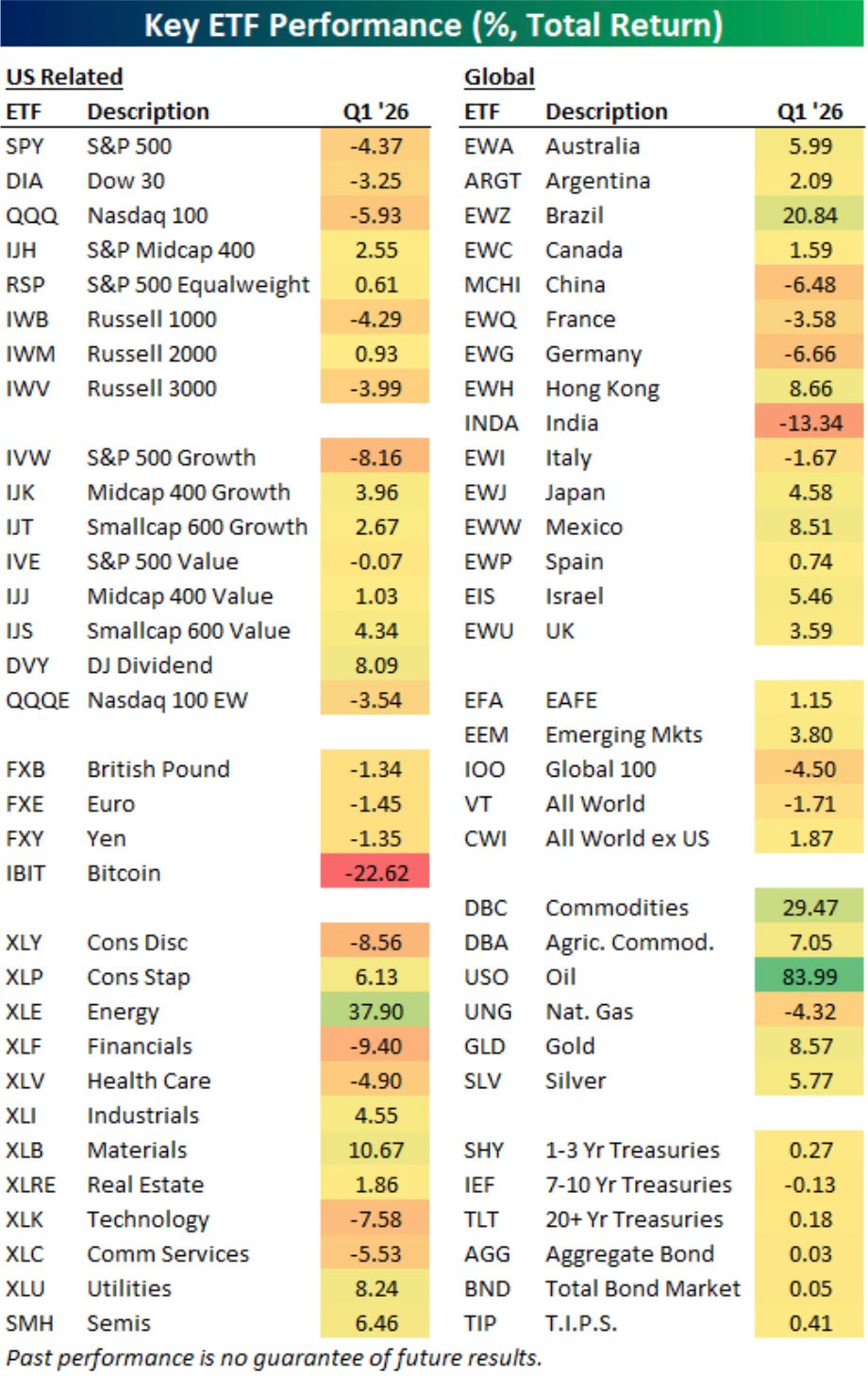

If you had told investors in January that bitcoin would be the single worst-performing asset class by the end of March, most would have laughed. But here we are. Bitcoin dropped more than 23% while commodities ripped 30%. Large-cap U.S. stocks weren’t far behind bitcoin on the losers list. That’s not a lineup many saw coming.

Here’s what the damage looked like at the sector level. Energy was the clear standout. Everything else was mostly red.

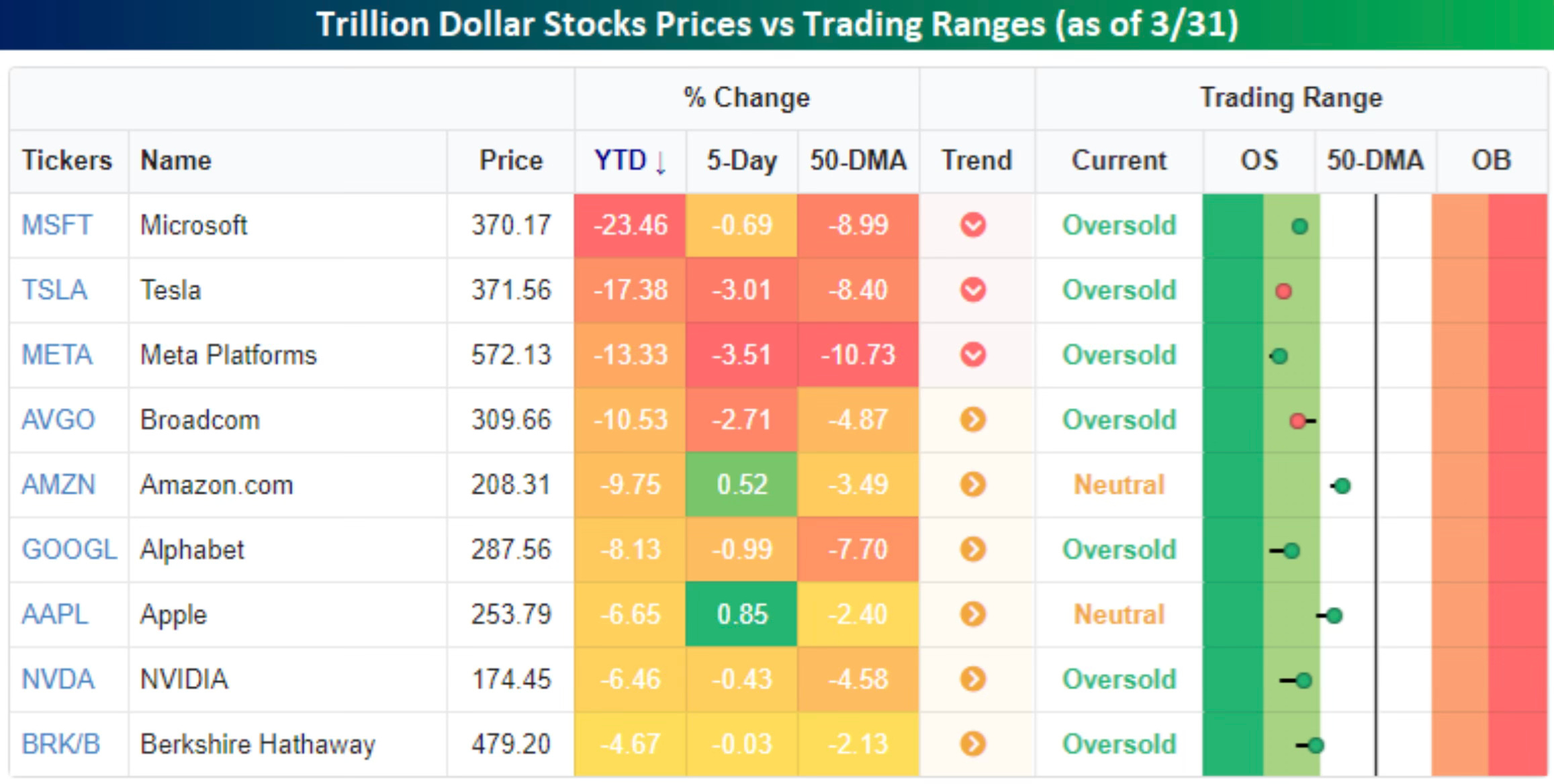

The megacaps didn’t just underperform the market. They led it lower. Microsoft is down more than 23% year-to-date. Tesla is off nearly 17%. Every name on this list is in the red. Most of them are sitting in oversold territory.

One notable split: small and mid-caps are still positive on the year. It’s the mega-cap weight dragging large-cap indexes down. The equal-weighted S&P 500 tells a very different story than the cap-weighted one.

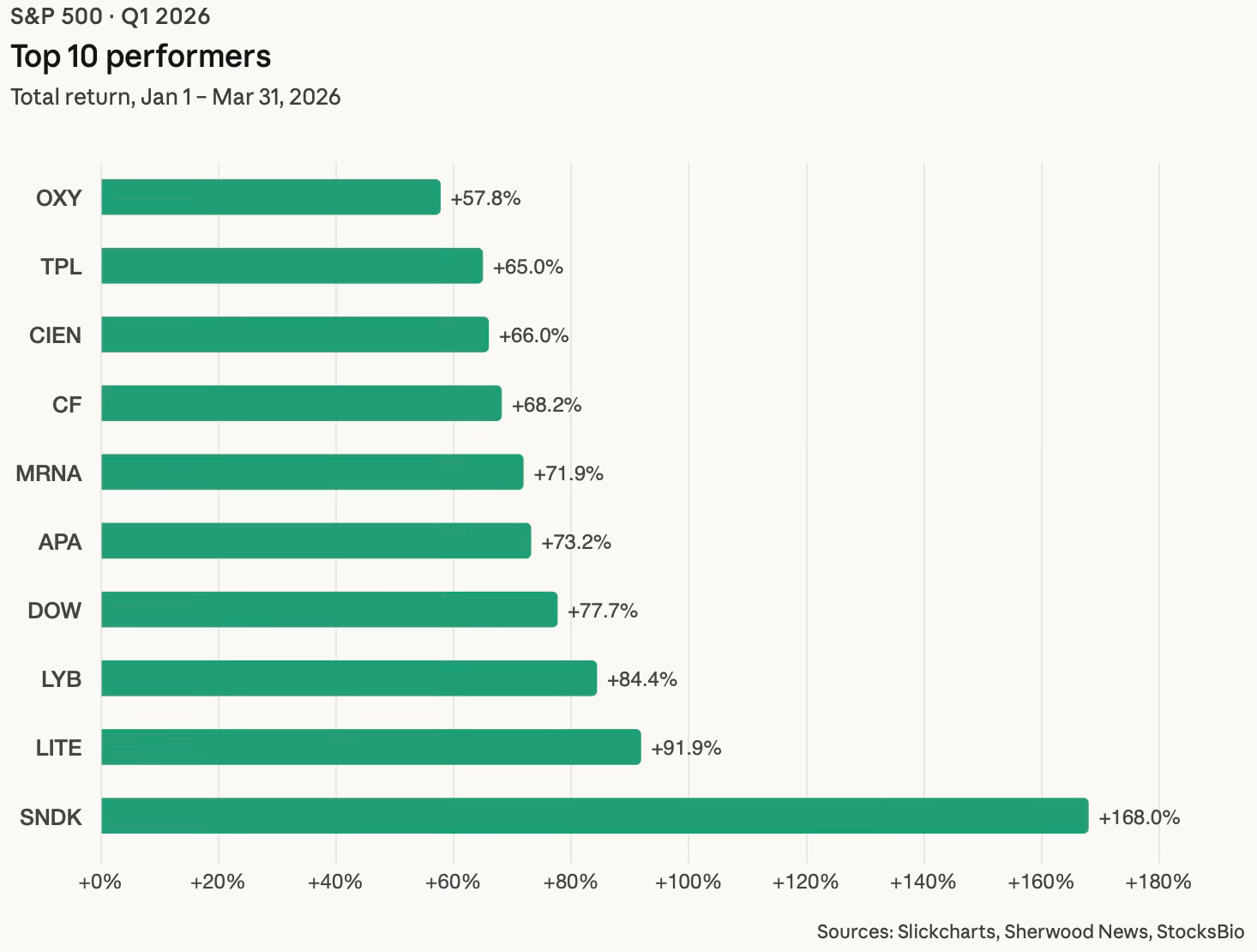

The top performers this quarter tell a story about two things: memory chips and oil.

Sandisk finished Q1 up 168%. It topped the entire S&P 500 in 2025 at +559%, and it’s apparently trying to do it again. No stock has ever topped the index back-to-back. It’s fueled by hyperscaler demand for flash storage in AI data centers. The broader memory and optical group followed its lead. Lumentum was up 92%. Ciena up 66%. Western Digital up 57%.

The other big winner was energy. The Iran conflict pushed crude well above $100 a barrel and 15 of the top 30 performers in Q1 were energy or chemical names. APA up 73%. OXY up 58%. Valero up 52%. It was the best quarter on record for energy stocks relative to the S&P 500.

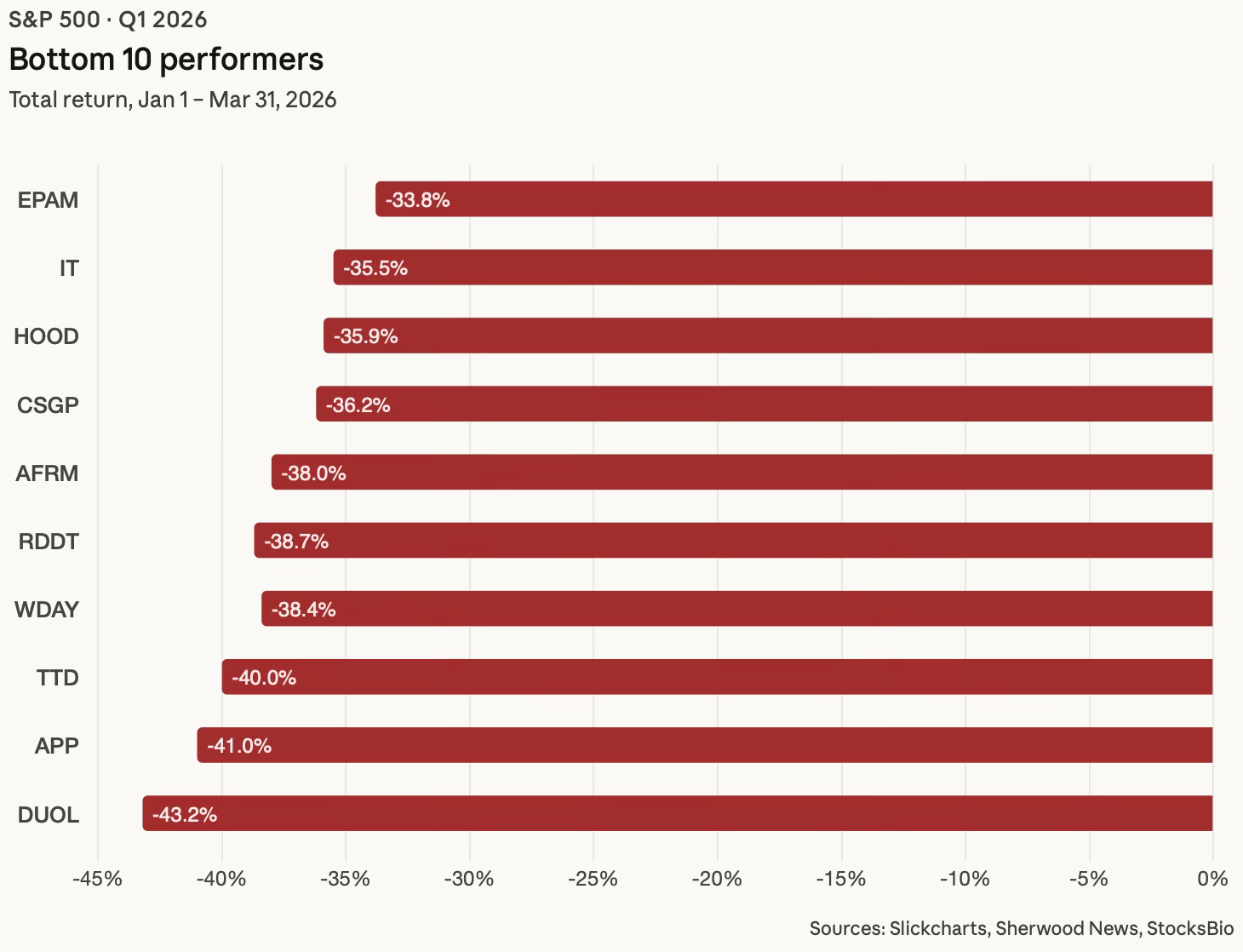

The losses were concentrated in software. Investors spent most of the quarter asking a simple question. If agentic AI can do the work, why pay for the enterprise software?

That fear alone crushed some of the biggest names from 2025. Software companies made up more than half of the bottom 20 performers in Q1. Trade Desk dropped 40%. Workday fell 38%. Adobe was off 31%. Salesforce down 30%. AppLovin, which surged 108% in 2025, was the single worst performer in the index this quarter, falling 41%.

The Q1 story is clear. What happens next is the harder question. Paid subscribers get the full Q2 outlook, a look at what the technicals are saying, and a breakdown of today's jobs report below.