Investing Update: Is a Recession Still Coming?

What I'm buying, selling & watching

Both the S&P 500 and Nasdaq finished down for the week. The S&P 500 had been down 3 straight sessions and the Nasdaq down 4 straight sessions until both streaks were broke on Friday. This came after we just saw multiple day winning streaks for both the week prior.

Even with the ups and downs the Nasdaq still remains on the track for its best year ever.

The S&P 500 also remains up over 16% YTD.

The Year End Rally?

Where does this leave the path into year-end?

September is traditionally one of the weaker months of the year throughout history. But as Ryan Detrick points out, that’s different after the S&P 500 is up big during the first 7 months of the year.

When the S&P 500 is up 15% or more after 7 months and down in August, like it just was this year. September has been higher 8 out of 9 times and the rest of the year has never been lower.

We’re also in the tail end of the election cycle which I’ve talked about multiple times. This chart shows the last 10 pre-election years dating back to 1983. As you can see there is historically a down August. That’s then followed by a spike in early September and a fall late in the month, which then historically sets up a rally into year-end.

What would spur a rally into year-end when we already have giants gains in both the S&P 500 and Nasdaq?

The catch up trade or the great chase could be the fuel to drive the market higher. With as many managers as this market rally caught offsides, we could very well see them play catch up. That’s because most everyone was extremely bearish to start 2023 and weren’t positioned for this run up in stocks. If managers or funds are lagging, they have to make up ground fast before the end of the year.

I’ve wrote about the momentum shifting more bullish and you’ll see more evidence of that below. If this surge into the end of the year is to happen, I will be watching the high beta stocks and risk on assets in the coming weeks. If those start catching a bid higher, we very well could see a run higher into year end. Keep in mind the S&P 500 is still only 7.6% away from the all-time high of 4,796. I wouldn’t rule out a new all-time high in 2023 just yet.

Bulls Roar

In my last update, Investing Update: Has Momentum Shifted? I had indicated how momentum had been looking like it’s shifting more bullish. The new sentiment reading shows just that. In fact, the bullish sentiment took a giant leap. Investors are seeing green ahead.

Is a Recession Still Coming?

I know, I know that darn word recession is still hanging around. I thought I was done talking about it also. But when data and information comes up, I have to discuss it.

First off, the number of companies saying the word recession during earnings calls fell for the 4th straight month to 62 in Q2. That’s the lowest number of times it has been mentioned since Q4 2021.

On the other side of that, we also continue to hear how the yield curve is inverted. What does that mean and why is that so important?

For over a year we’ve had what’s known as an inverted yield curve. That means the interest paid by 10-year Treasury bonds has been lower than shorter-term debt, like two-year Treasurys. Short-term interest rates are higher than long-term interest rates.

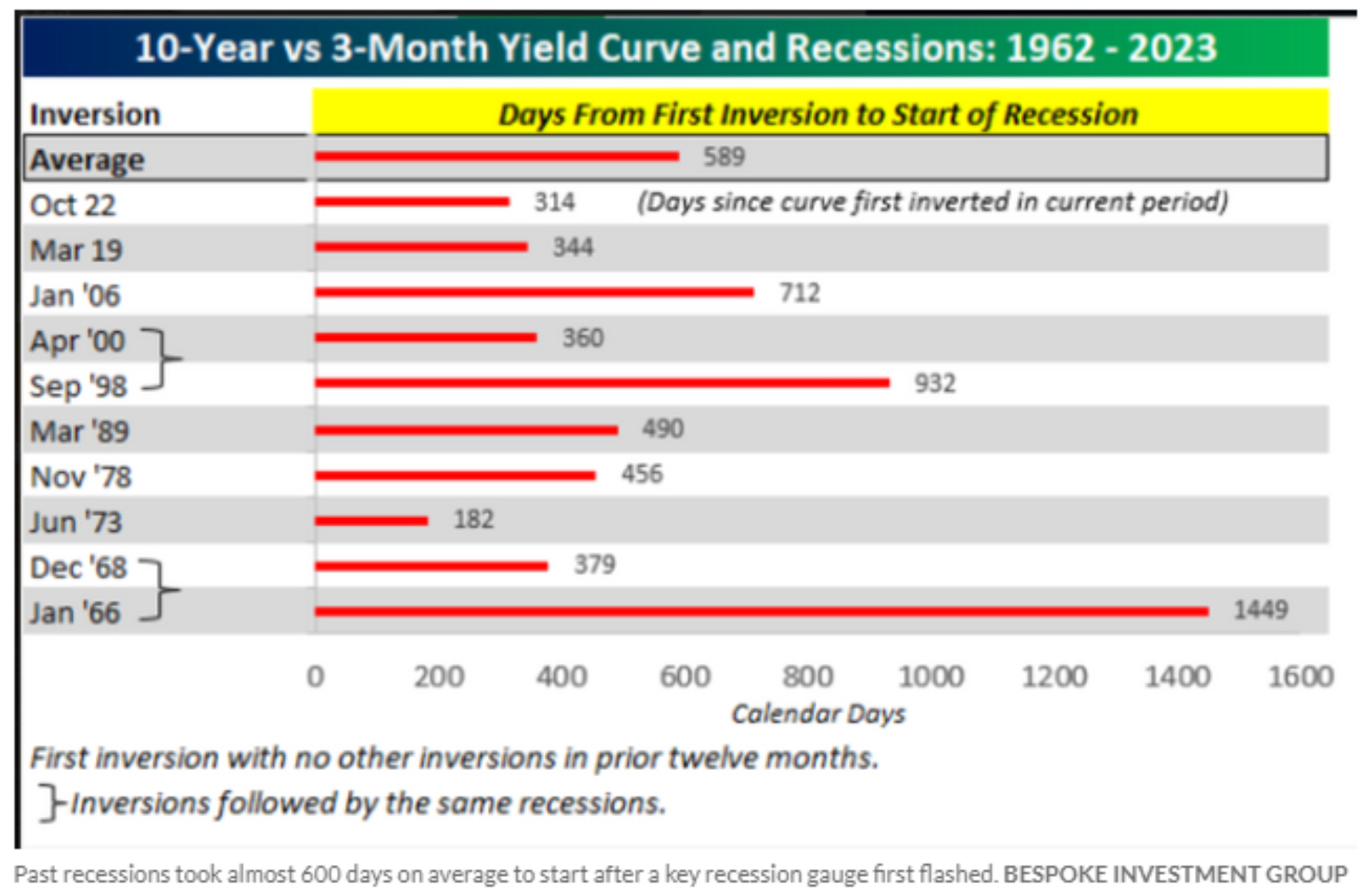

The history of inverted yield curves has been a very reliable indicator that a recession is likely. The following is from the team at Bespoke and they have such a beautiful chart to illustrate their findings.

Since the early 1960s, recessions took an average of 589 days to appear after the 10-year and 3-month treasury yield curve inverted. This means that the next recession could materialize around June 2024.

This then comes from Liz Ann Sonders.

Spread between 10y and 3m Treasury yields has been negative for 218 consecutive days as of yesterday … now officially longer than streak that ended in 2007, and longest since streak that ended in 1980

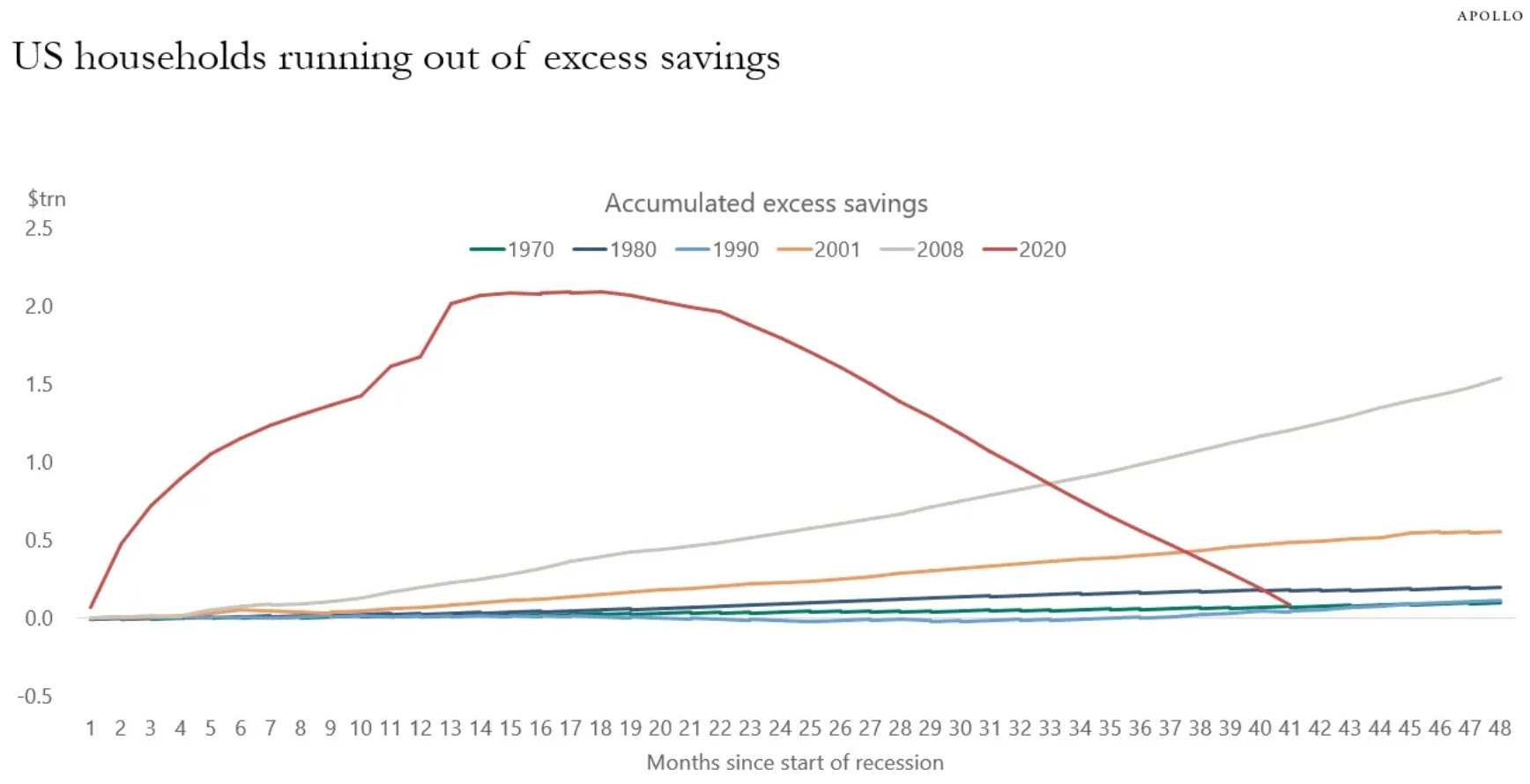

Lastly we have an update on where household savings is at from Apollo’s chief economist Torsten Slok.

We have updated our estimates of how much excess savings households have left using the Fed’s methodology, and the conclusion is that consumers are almost out of pandemic savings, see chart below.

As we know, consumer spending is responsible for 70% of GDP. If the U.S. consumer stops or even pulls back spending, we know what that results in. I personally don’t think we get to that point or serious about a recession until the unemployment rate starts to climb. With the unemployment rate still at 3.8%, we need to see it start to approach 5% before recession becomes a true possibility in my view.

This chart does a good job showing the link between the unemployment rate to recessions throughout history.

Maybe this time is different. Or maybe it isn’t. Regardless, we’re going to continue to hear about it and the recession word lives on.

Moves I’ve Made

Deere DE 0.00%↑ This week I added to my position in Deere at $406 a share. They recently boosted their dividend by 8%. It’s the second dividend raise for them in 2023. They had a good earnings report last month. I thought the stock should have been up after it beat and raised. Not down. It’s still lower from where it was before it reported

The stock is down 5.8% so far in 2023. This was one of my stock picks for 2023 and you can read about why I originally started my position here, Investing Update: 3 Stocks For 2023. I’m still very bullish this name long term and if it does go lower, I’ll buy more.

It’s also interesting to me to the extent that China is stockpiling the important food reserves. They now hold 69% of the world’s corn reserves, 60% of the world’s rice reserves and 51% of the world’s wheat reserves. As the U.S. talks about the need for on-shoring and the ongoing concerns regarding China, there aren’t many things more important than food. The farming and growing food infrastructure of the U.S. is Deere.

The Coffee Table ☕

Kelly Evans had a great post on China and how it has powered returns for businesses and investors for years, but it’s now turning into a liability. Why China is turning into a liability for American companies. This was very evident this week with the news regarding the issues between Apple and China. Companies with high China exposure have been underperformers. It will be interesting to see where this road leads.

I enjoyed reading Jesse Cramer’s post called The Most Frustrating Phrase in Personal Finance. The word “it depends” is frustrating to hear and say, but everyone’s situation regarding their investments, personal finance and life can vary so widely from one person to another. There just isn’t a correct answer for every financial situation or question that fits everyone.

Richard Quinn wrote a post on something that I’ve long believed and told others. He wrote the same two exact sentences I’ve said. “It’s okay to spend money on things you enjoy. If you’re spending on things that make you happy, you shouldn’t feel guilty.” This was good a good reminder why you should spend on what you want and not care about what others think. My Car Journey

Tim Ferriss shared the following quote last week. It dates back to 1844 and it still really speaks volumes.

“Anxiety is the dizziness of freedom.”

-Soren Kierkegaard

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.

Disclaimer: This is not investment advice. You should not treat any opinion expressed as a specific inducement to make a particular purchase, investment or follow a particular strategy, but only as an expression of an opinion. Do your own research.