Follow The Money

The AI buildout isn't slowing down. It's accelerating.

We just heard from the four largest technology companies on earth. And if you listened closely, the message was identical across all of them. We are not slowing down.

This week, Microsoft, Meta, Alphabet, and Amazon all reported Q1 2026 earnings. The numbers were extraordinary. The commentary was even more important.

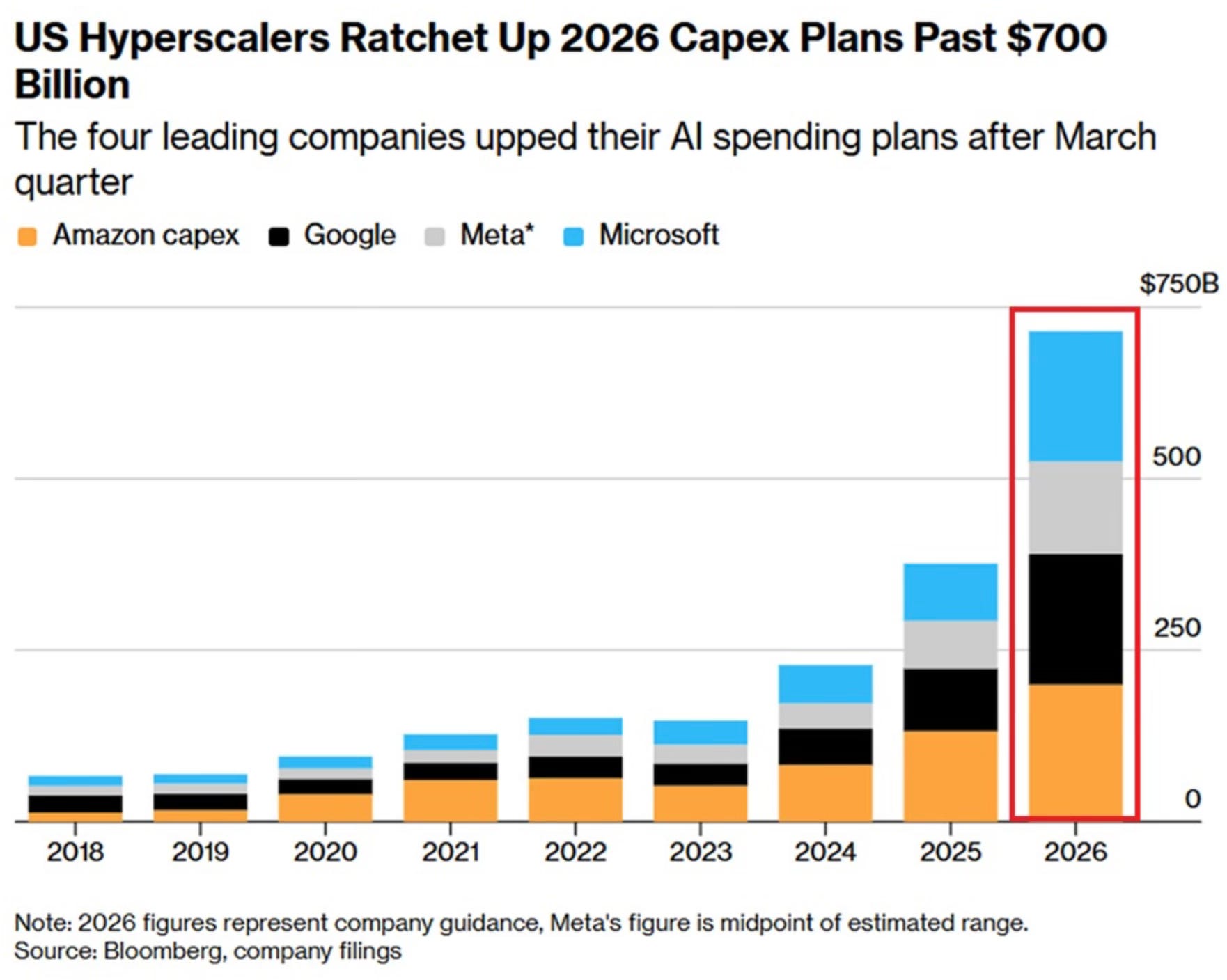

Combined, these four companies are now on track to spend more than $700 billion in capital expenditures in 2026 alone. That’s nearly double what they spent last year, and $100 billion more than they had projected just one quarter ago.

Let that sink in for a second.

$700 billion. In a single year. On AI infrastructure.

That’s more than the GDP of most countries. And the pace is not leveling off. It’s picking up.

What They Said. Straight From the Earnings Calls

This isn’t about stock tips. It’s about listening. These CEOs and CFOs are telling you exactly what is happening. The question is whether you’re paying attention.

Microsoft (MSFT)

Satya Nadella did not mince words on the call:

“We are focused on delivering cloud and AI infrastructure and solutions that empower every business to eval-max their outcomes in the agentic computing era. Our AI business surpassed a $37 billion annual revenue run rate, up 123% year-over-year. We are at the beginning of one of the most consequential platform shifts that will change the entire tech stack as we move from end-user driven workloads to workloads driven by end-users and agents. This will drive TAM expansion and change the value creation equation across the entire economy.”

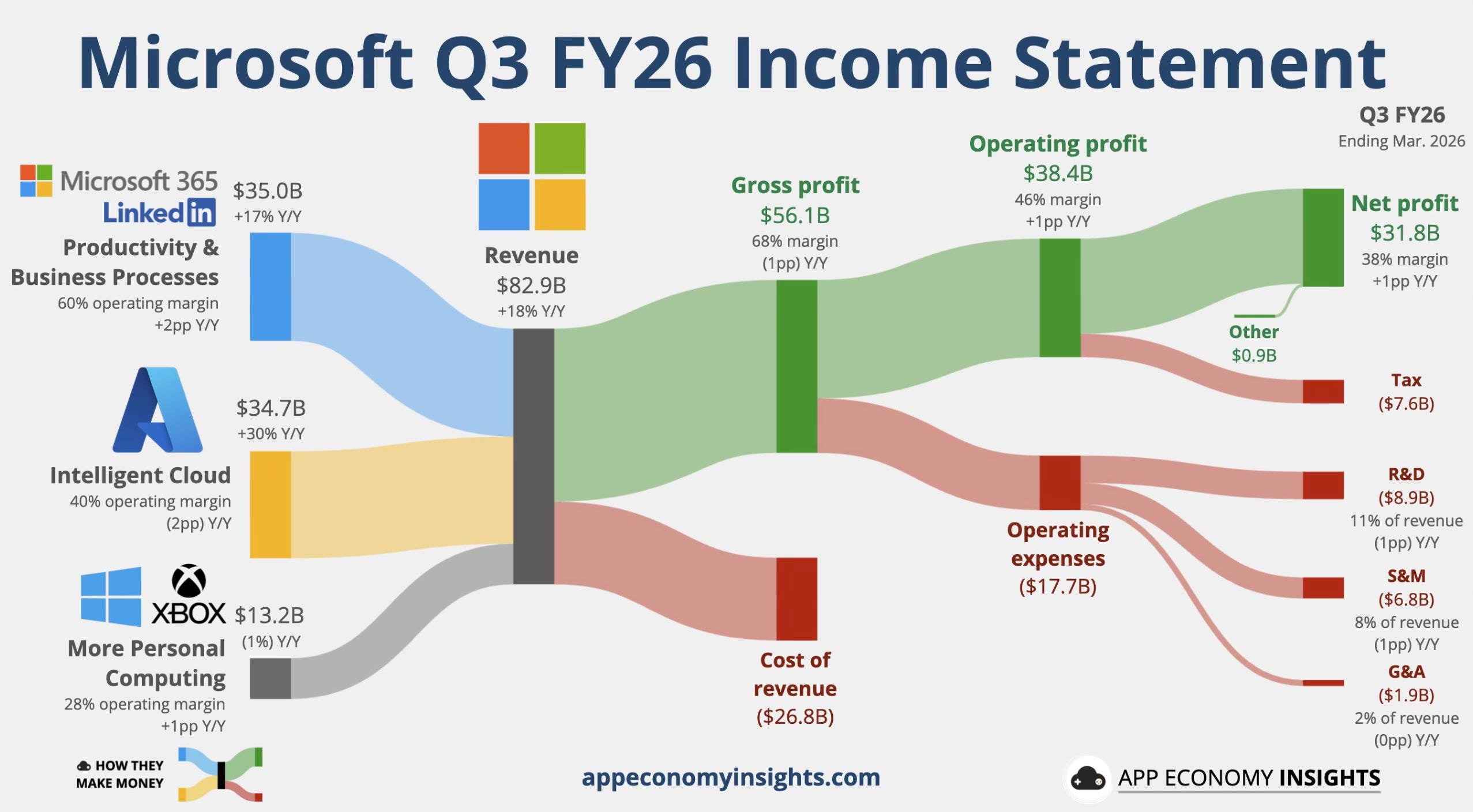

Microsoft added one gigawatt of AI infrastructure capacity in a single quarter. CFO Amy Hood said the company expects to spend over $40 billion in Q4 alone, and the full-year capex bill lands at approximately $190 billion . Roughly $25 billion of that is driven by higher component pricing alone. She also made a remark that should stop every skeptic in their tracks. AI margins are already better than cloud margins were at the same stage of development.

Azure grew 40% year-over-year. The company extended its exclusive Azure agreement with OpenAI through AGI or 2030, with OpenAI contracting an incremental $250 billion of Azure services not yet reflected in current results. Microsoft’s commercial remaining performance obligation. Which is its total contracted future revenue, hit $627 billion, up 99% year-over-year.

Azure remains capacity constrained. Demand is beating supply. That’s not a problem. That’s a signal.

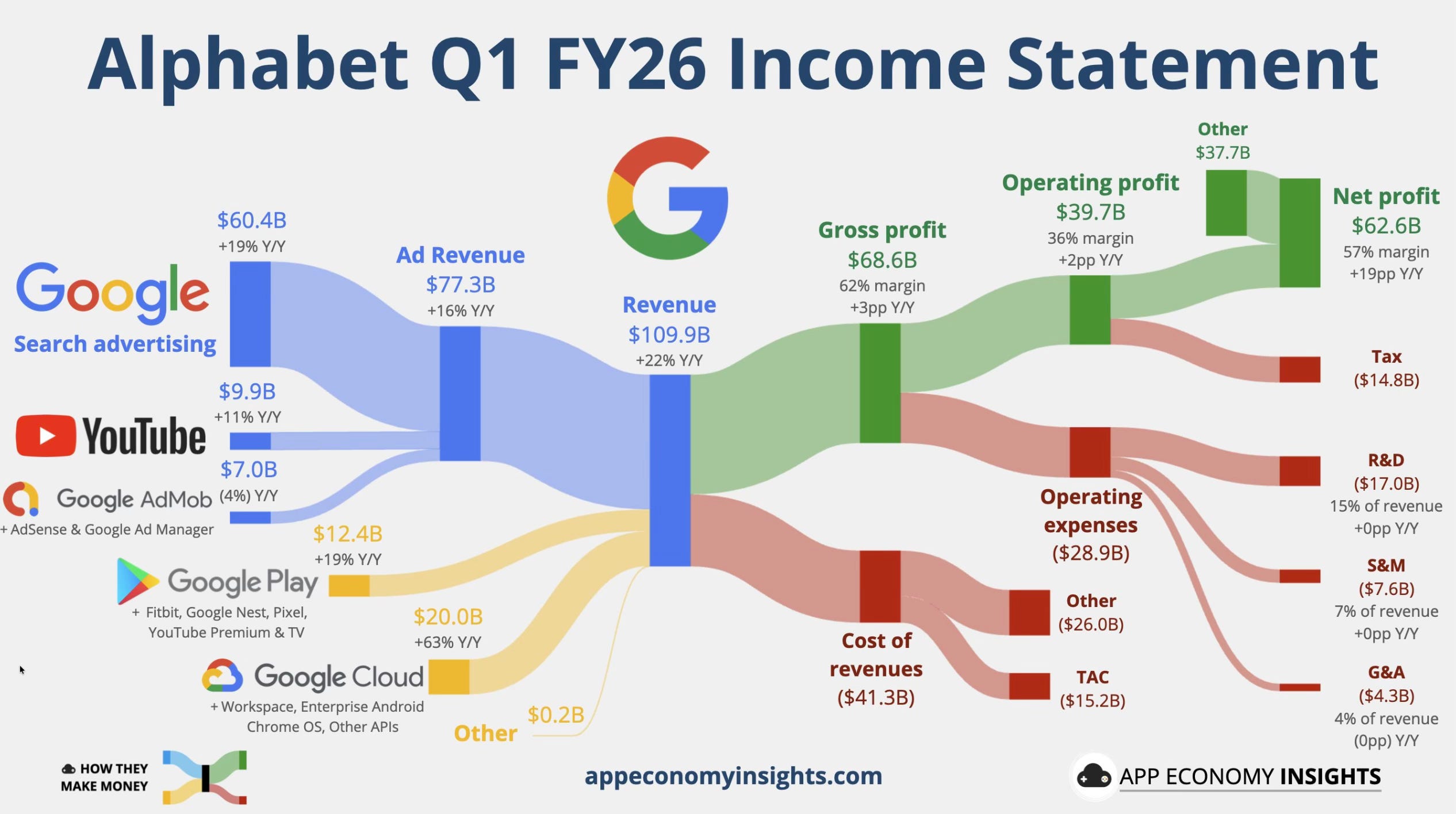

Alphabet (GOOGL)

Sundar Pichai’s opening line set the tone.

“It was a terrific quarter for Alphabet. Our AI investments and full-stack approach are lighting up every part of the business.”

Google Cloud grew 63% year-over-year, exceeding $20 billion in quarterly revenue for the first time. Cloud backlog nearly doubled sequentially to $462 billion. Then CFO Anat Ashkenazi said something that every investor needs to hear.

“We are seeing unprecedented internal and external demand for AI compute resources.”

She also delivered the most important forward-looking signal of the week. Alphabet expects 2027 capex to significantly increase compared to 2026.

Pichai noted that Alphabet is compute constrained in the near term and that cloud revenue would have been higher if we were able to meet the demand. Think about that. The business would be bigger if they could build faster. This is a supply problem, not a demand problem.

Here is perhaps the most remarkable data point from the entire week of earnings. Pichai disclosed that nearly 75% of all new code written at Google is now AI-generated. It’s reviewed and approved by engineers, but generated by AI.

That number was 50% just last fall. This is not a hypothetical future productivity benefit. It’s happening right now, inside the walls of one of the most sophisticated engineering organizations on earth. AI productivity is not ahead of us. It’s already here.

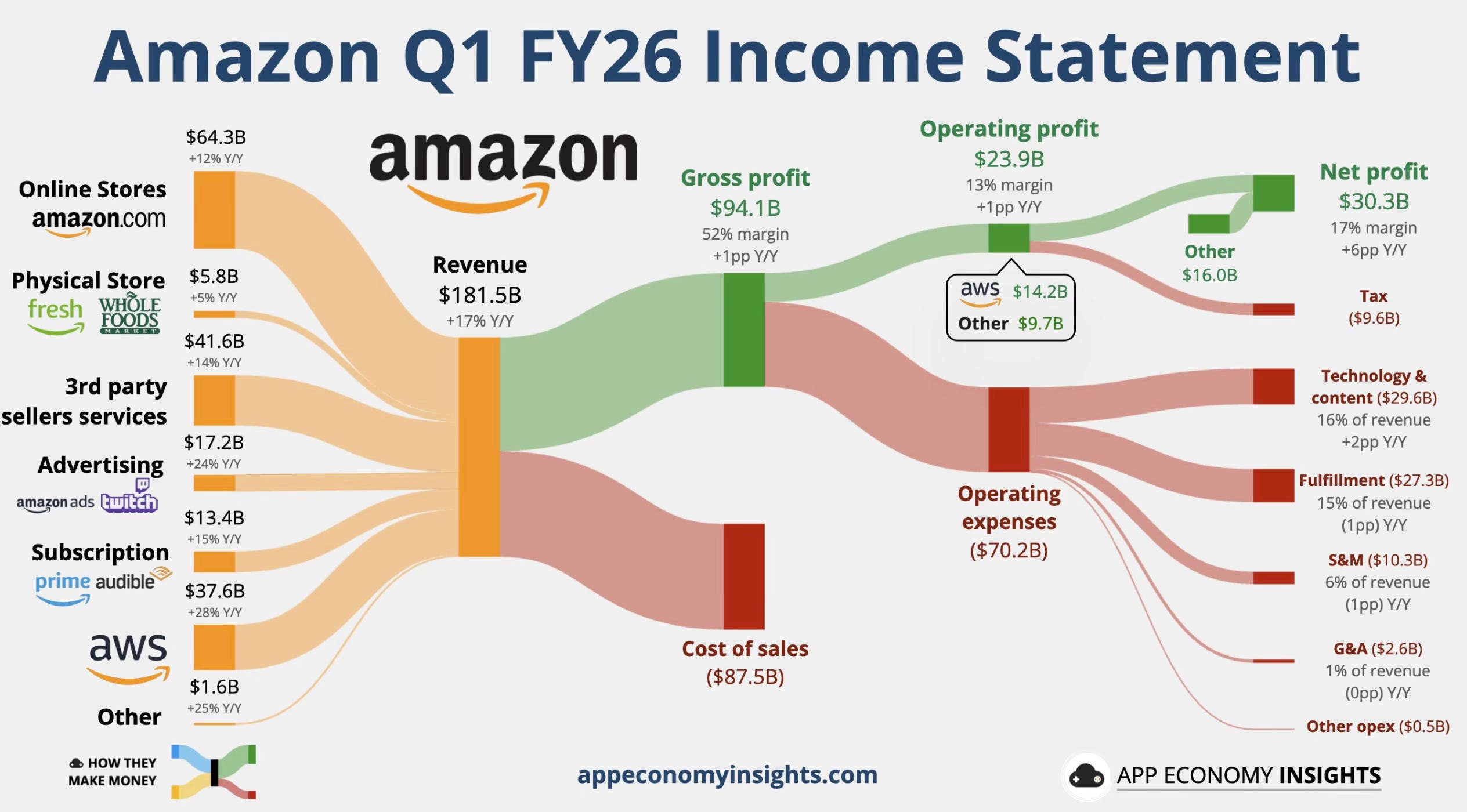

Amazon (AMZN)

Andy Jassy delivered what may have been the most quotable moment of the entire earnings season. Then he later reinforced it on CNBC:

“We’ve never seen a technology grow as rapidly as AI. Three years after AWS launched, it had a $58 million revenue run rate. In the first three years of this AI wave, AWS’s AI revenue run rate is over $15 billion — nearly 260 times larger. We believe AI is the biggest technology transformation in our lifetimes. It’s going to reinvent every single customer experience we know. When you have shifts that are this momentous, you want to bet big.”

AWS grew 28% year-over-year, its fastest growth in 15 quarters. It’s now a $150 billion annualized revenue run rate business. Amazon’s chips business crossed a $20 billion revenue run rate, growing triple digits year-over-year.

AWS backlog? $364 billion and that doesn’t include the recently announced Anthropic deal worth over $100 billion.

Jassy’s framing on capex was direct. Amazon invests 6-24 months before billing customers. They have high confidence the 2026 capex will be monetized well, with customer commitments for a substantial portion already in place.

Q1 cash capex alone was $43.2 billion.

Meta (META)

Mark Zuckerberg’s headline quote:

“We had a milestone quarter with strong momentum across our apps and the release of our first model from Meta Superintelligence Labs. We’re on track to deliver personal superintelligence to billions of people.”

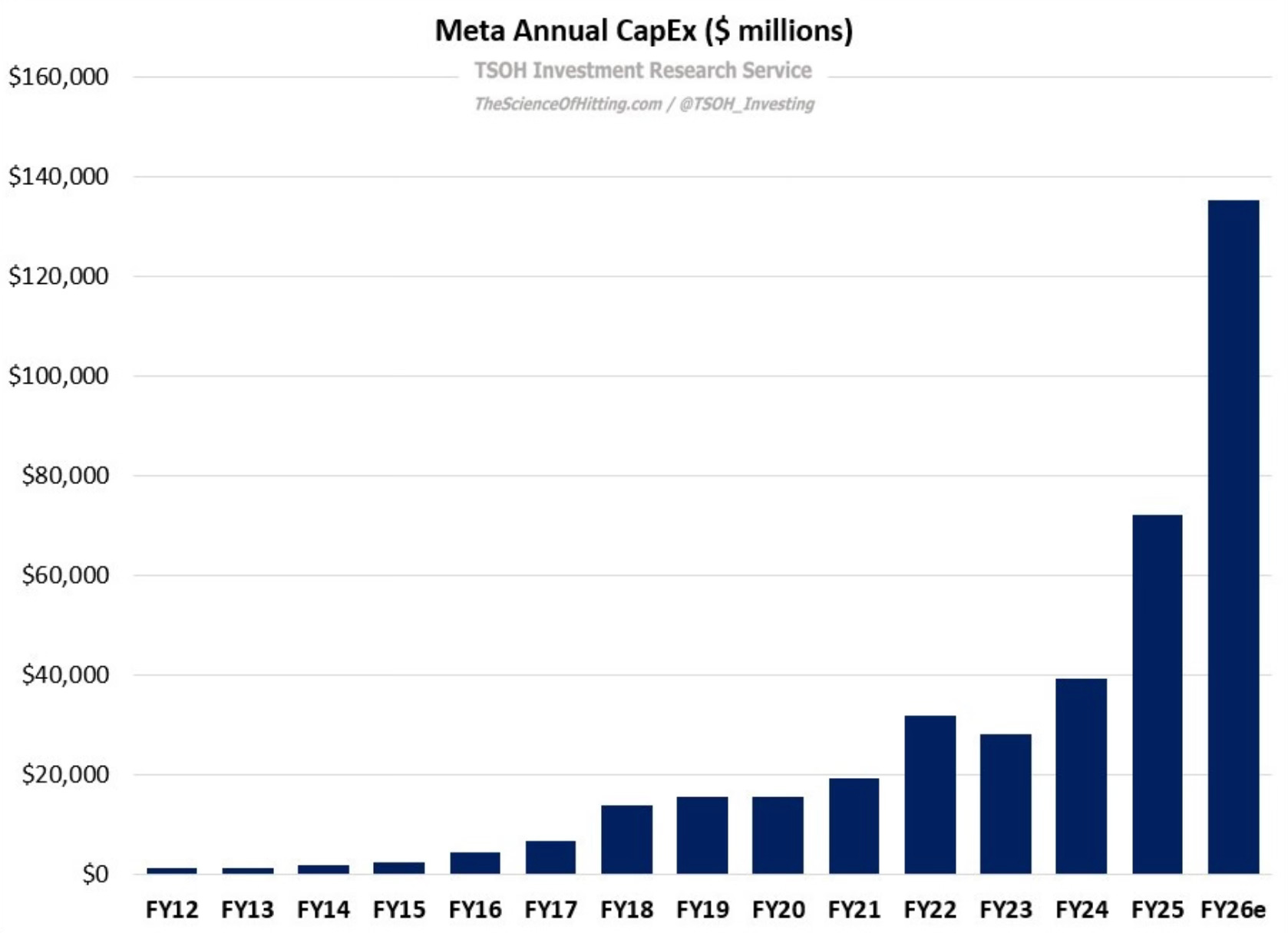

Revenue was $56.3 billion, up 33% year-over-year. The company’s fastest growth since 2021. Meta raised its 2026 capex guidance to $125–$145 billion, up from $115–135 billion, driven in part by surging component costs including memory.

To put that visual in plain terms: Meta is now planning to spend more on AI in 2026 than it spent in the previous two years combined. And here is a detail that tells you just how acute the demand is. Meta is now extending the useful life of some data center servers from 6 years to 7 years due to what an internal memo called a “significant server supply deficit” caused by memory chip shortages.

The company did not anticipate the hardware demand growth it’s seeing. That’s not a red flag. That’s confirmation that demand is running hotter than even these companies expected.

Zuckerberg has been crystal clear. As more capital flows toward AI hardware, there is less available for headcount. The 8,000 layoffs announced this week are not financial distress. They are a deliberate reallocation of capital toward the AI race.

The stock has dropped on the capex bump. My view is that’s the market misreading the signal.

What These Four Businesses Look Like Today

Four companies. Four different business models. One shared conviction. Every single one of them is doubling down on AI infrastructure regardless of what it costs in the near term, because they all see the same thing on the other side.

The Numbers That Put It All in Perspective

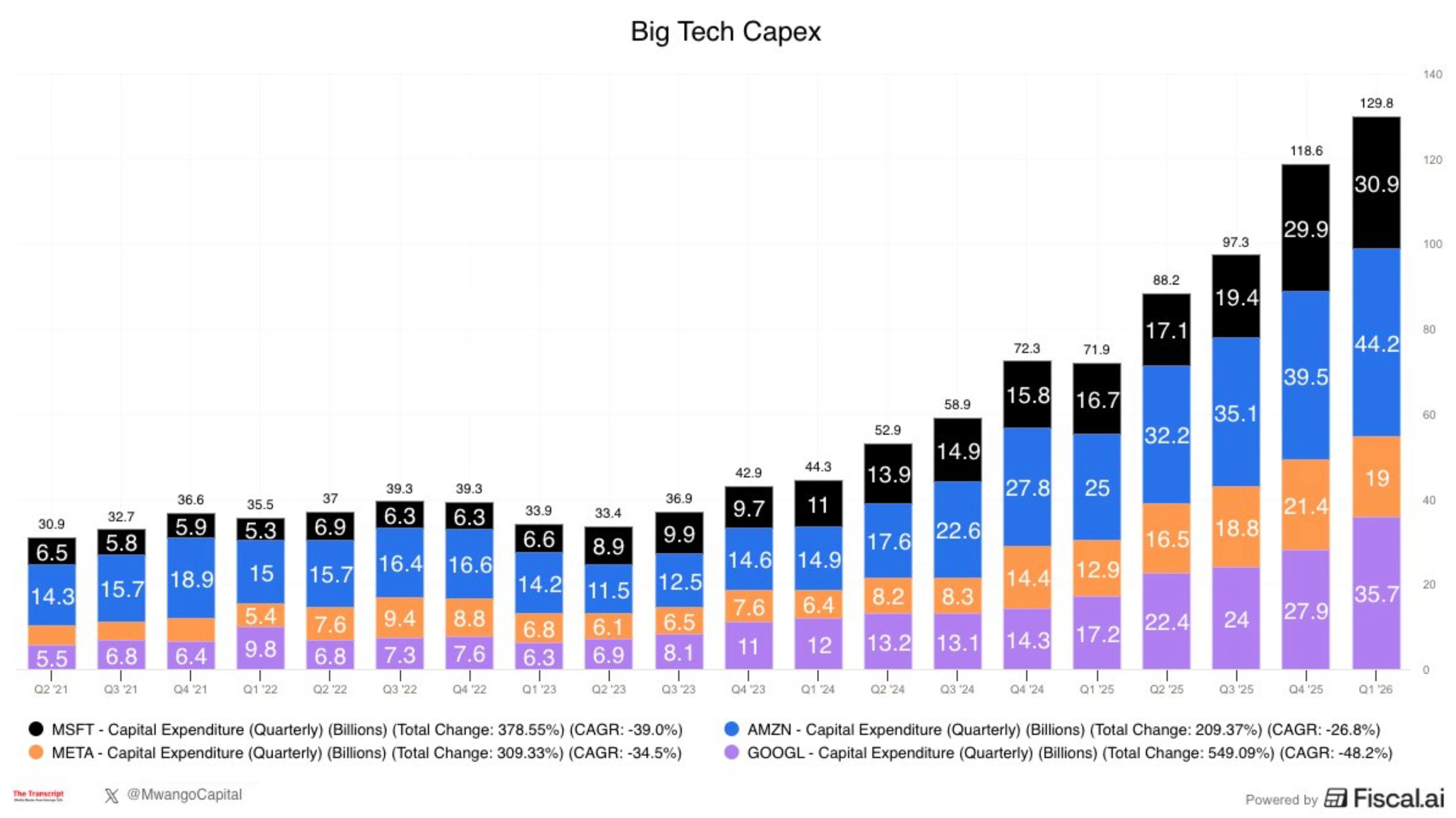

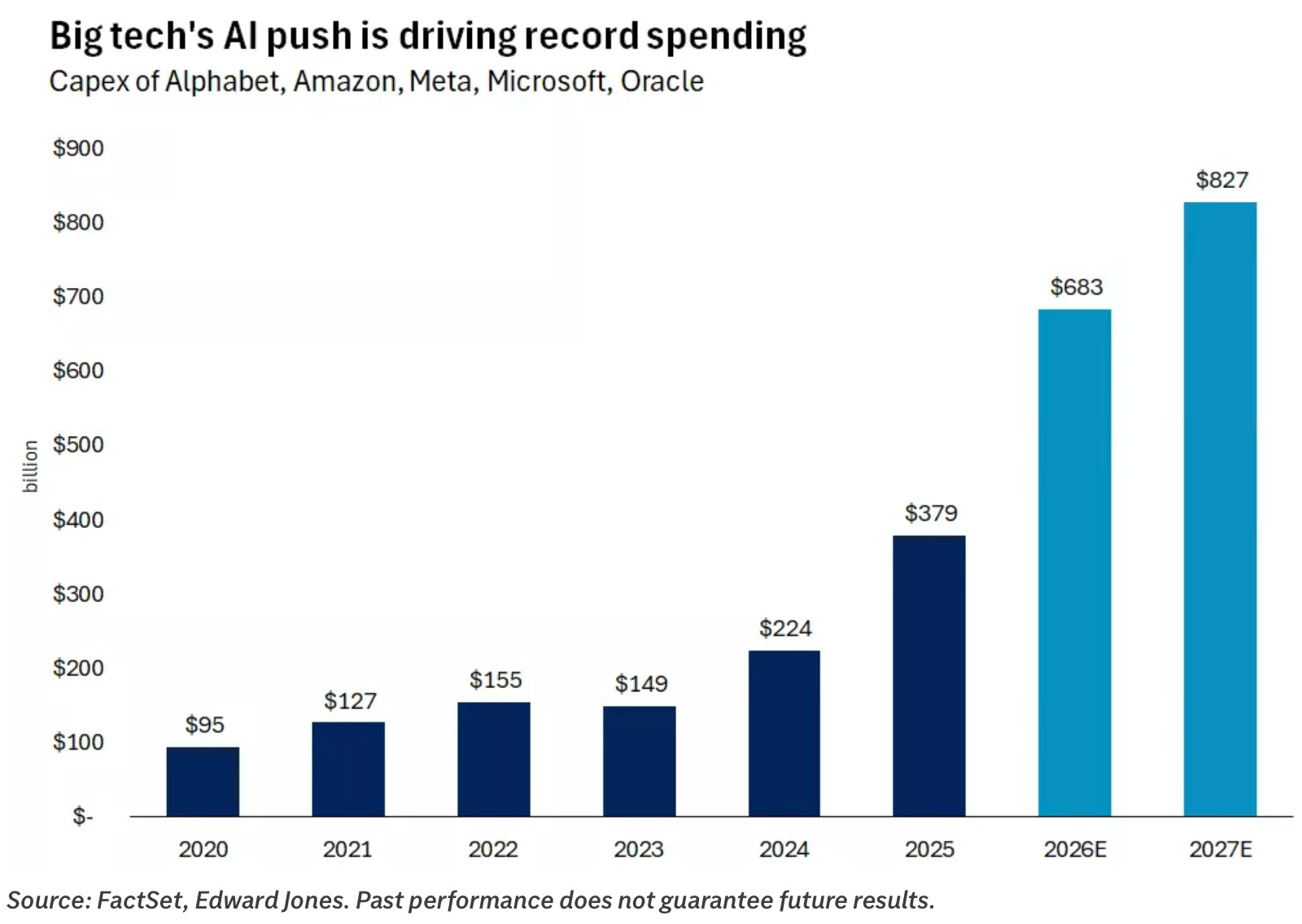

Here is what $700 billion in AI capex actually looks like on a quarterly basis, company by company, stretching back to 2021.

The acceleration in that chart is not subtle. Q1 2026 alone, only one quarter, was $129.8 billion combined. Two years ago, that was a full-year number.

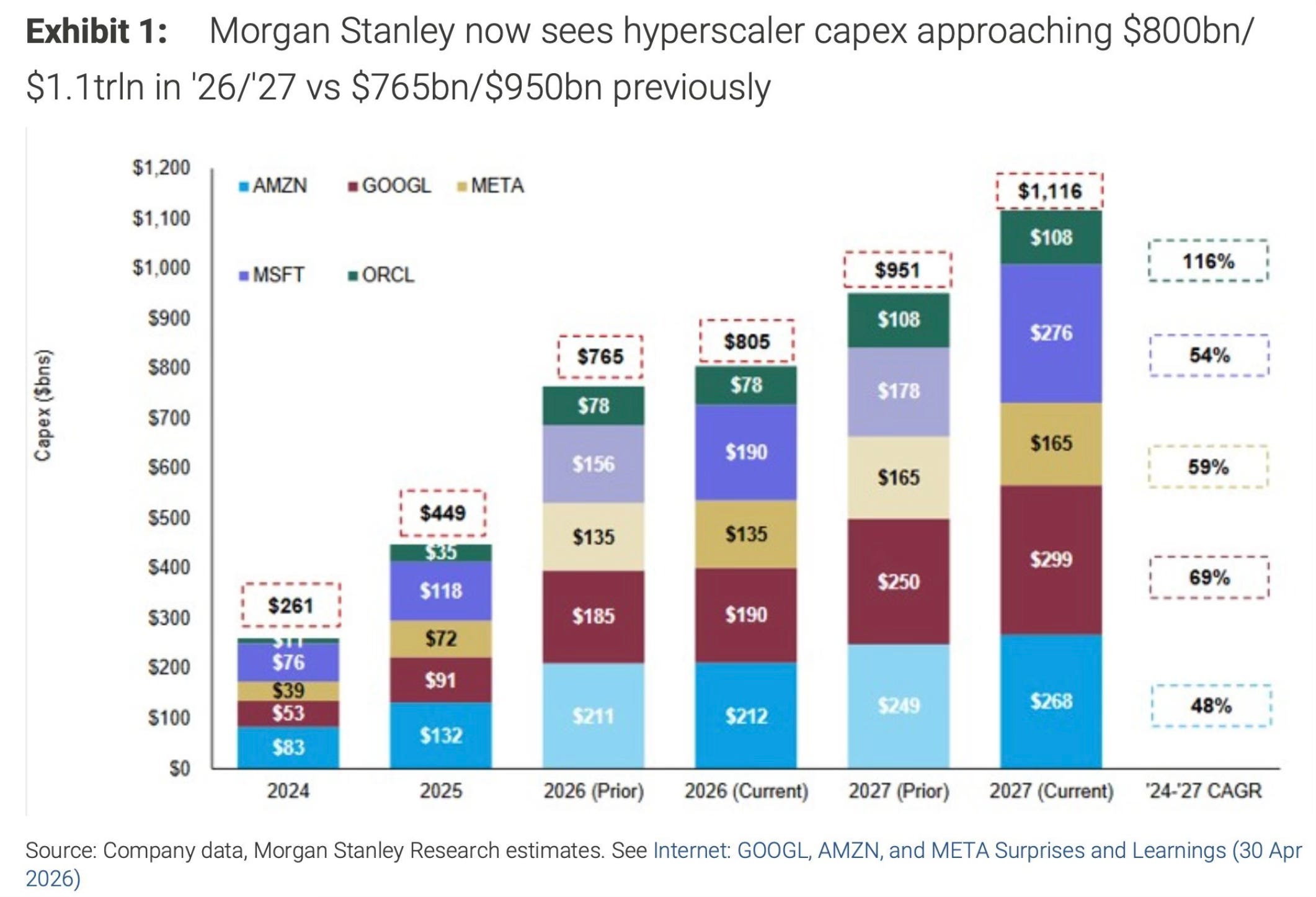

Now here is the part that should really get your attention. Morgan Stanley, after this week’s earnings, has again raised its hyperscaler capex forecasts. They now expect these five companies to spend approximately $805 billion in 2026. That’s up from their prior estimate of $765 billion. And for 2027? Morgan Stanley now sees the number crossing $1.1 trillion.

One trillion dollars. On AI infrastructure. In a single year.

To put the trajectory in even sharper relief. This is what the five-year arc looks like when you zoom out.

In 2023, these companies spent $149 billion combined. The 2027 estimate is $827 billion. That’s not a trend. That is a structural shift in how the global economy allocates capital.

AI Productivity Is Ahead of Us, Not Behind Us

One of the most important takeaways from this earnings season is what didn’t happen.

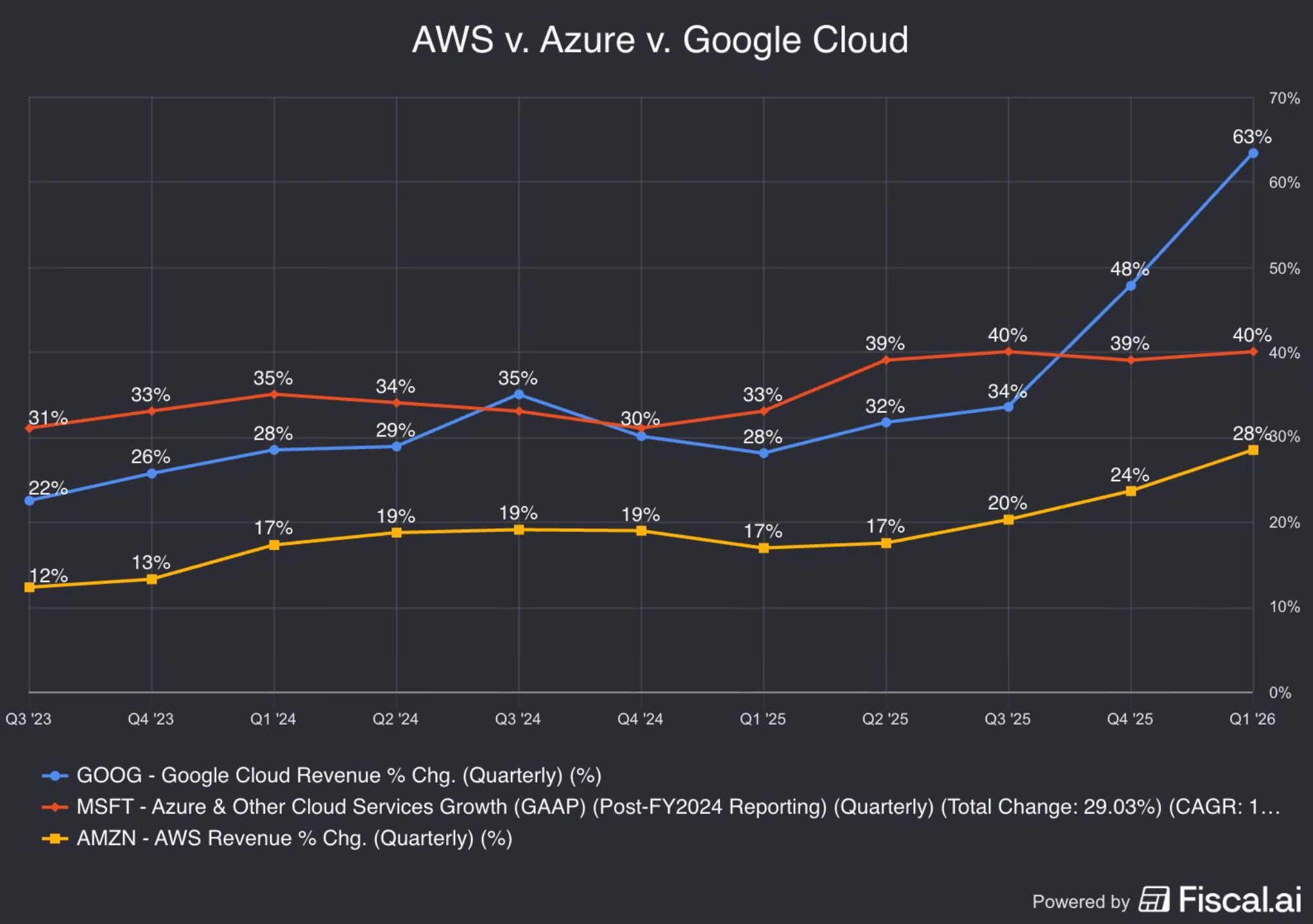

The bear case in that AI workloads have structurally lower margins than legacy cloud has been proven wrong. Cloud operating margins are expanding, not compressing, even as AI workloads scale. Google Cloud operating margin went from 17.8% to 32.9% year-over-year. AWS operating margin hit 37.7%.

Look at how cloud growth is accelerating, not decelerating, across all three platforms.

All three are reaccelerating. Google Cloud just hit its highest growth rate ever. The demand that was there in theory is now showing up in the revenue line.

This is still the buildout phase. The hyperscalers called out their need for more compute and noted that results could have been even better if more AI capacity had been available. This is not speculation about the future of AI. It’s the present day constraint on their businesses.

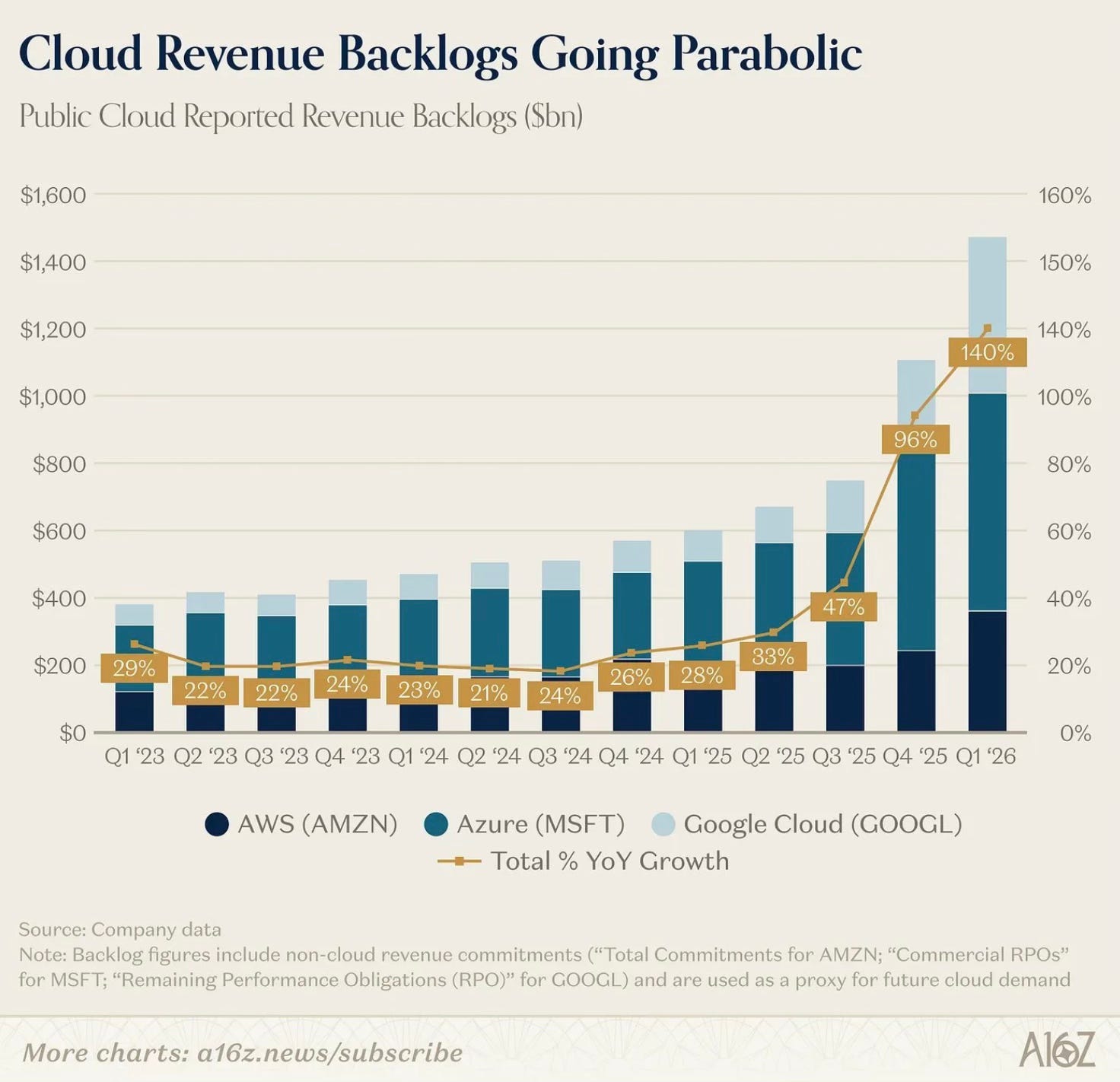

And it shows up in the backlog data too. Cloud revenue backlogs across AWS, Azure, and Google Cloud have gone parabolic. Now up 140% year-over-year combined. That is not a typo.

Back in my 2026 Outlook at the start of the year, I said we were in the third inning. I referenced a Bespoke survey at the time showing 46% of investors agreed. We’re still early in the cycle.

That view hasn’t changed. If anything, this week’s earnings calls confirmed it. The infrastructure is still being built. The monetization layer is just beginning to scale. The innings ahead of us are longer than the ones behind us.

I'm not just still bullish. I'm more confident than I was in January. But before we get to where I think the real opportunity sits, let's address the one question the bears won't stop asking because the answer is worth knowing.