Are 10% Mortgage Rates Coming?

The road ahead for mortgage rates

In just over two years, we have seen the 30-year fixed mortgage rate go from an all-time low of 2.65% in 2021 to now 7.8%. That’s the highest level since 2000.

This begs the question of when interest rates stop going up. Everyone was shocked once mortgage rates crossed 5%. Then there was no way we’d see over 6%. Now here we are with rates about to cross over 8%. Does this run continue even past 10%?

The Kobeissi Letter did a pole on X, where they asked, will mortgage rates hit 10% within 1 year?

Out of 2,810 votes, over 55% said yes. That was much higher than I anticipated. I voted yes.

As the Fed remains hawkish and rates continue to climb, we have to really ask, if we see 10% mortgage rates, can the housing market handle that? The housing market is already struggling with over 7% rates.

With the still high home prices and high mortgage rates, housing affordability sits at an all-time low.

That takes mortgage payments to where they are now.

This may be the best housing chart I’ve seen this year from Michael McDonough. The monthly mortgage payment for purchasers of existing homes, using the 30-year average mortgage rate, stands at $2,309. In March of 2020 it was $977.

How much home will that $2,309 mortgage payment currently get you? Not near what it could two years ago. A $700,617 house then, to now a $402,876 house. Soon it will be half the house as two years ago.

With most outstanding mortgages under 4% you can understand why the housing market remains frozen. Nobody wants to move and give up their historically low mortgage rate to take on a mortgage rate that is almost triple.

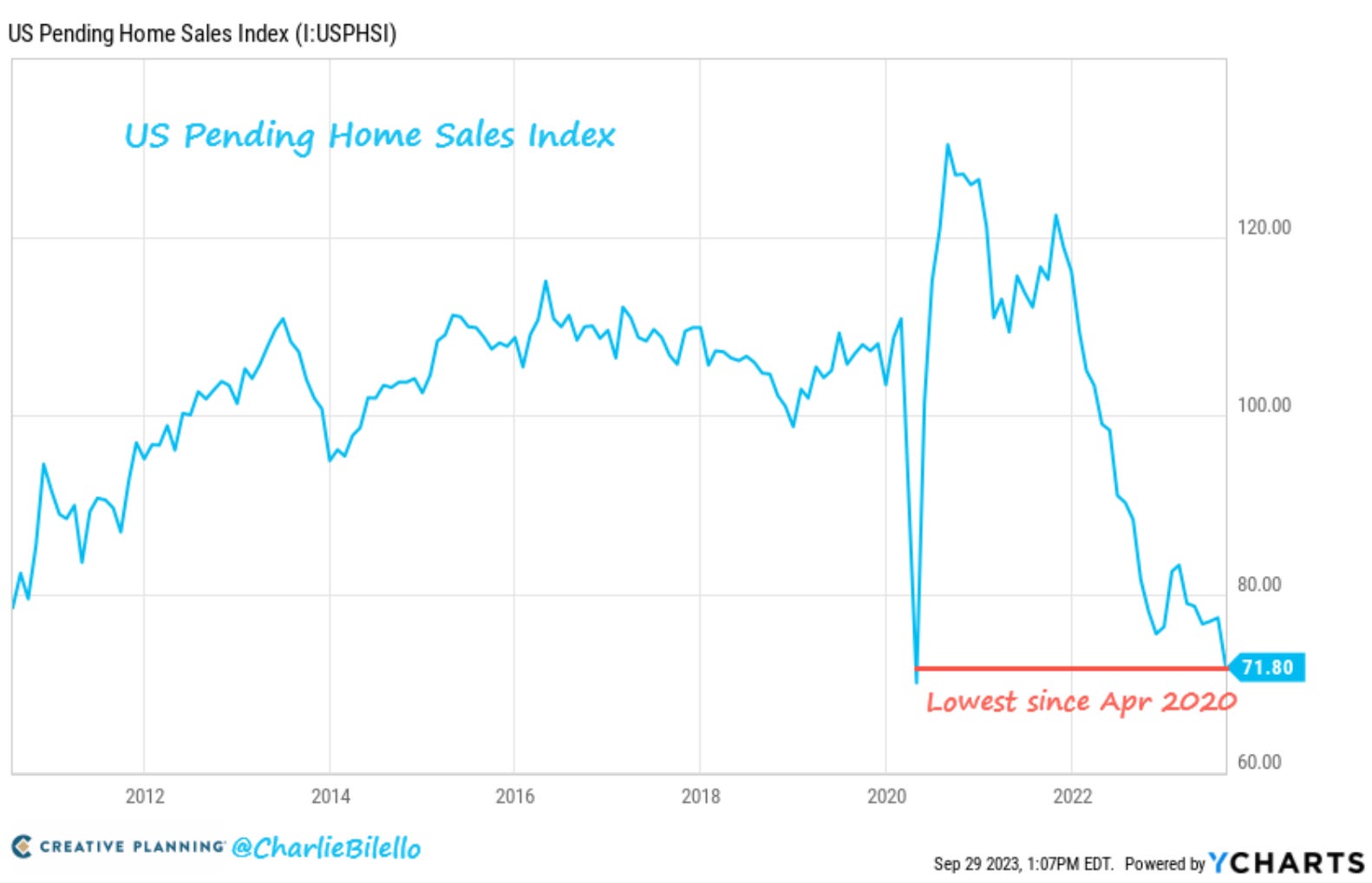

This has led home sales to exactly where you’d expect.

US pending homes sales hit the lowest level since April 2020. Remember, that was when the economy was essentially shut down due to the pandemic.

Redfin CEO Glenn Kelman summed up the housing market well in a recent CNBC interview.

"The only good thing right now about the US housing market is that it can't get much worse from here.”

"The only people who are moving are the ones who absolutely have to," Kelman added. "I wouldn't call that a Goldilocks scenario, I would call that rock bottom. But that's where we are right now, and the only relief is that it can't go much lower.”

If we’re at rock bottom now, what happens to the housing market if higher mortgage rates come? Is the housing market prepared for that?

Many seem to think rates start to ease. In the short-term that just doesn’t seem realistic with as hawkish as the Fed has been and what the 10-year treasury yield is doing.

While the Fed doesn’t set the interest rates that borrowers pay on mortgages, their actions influence them.

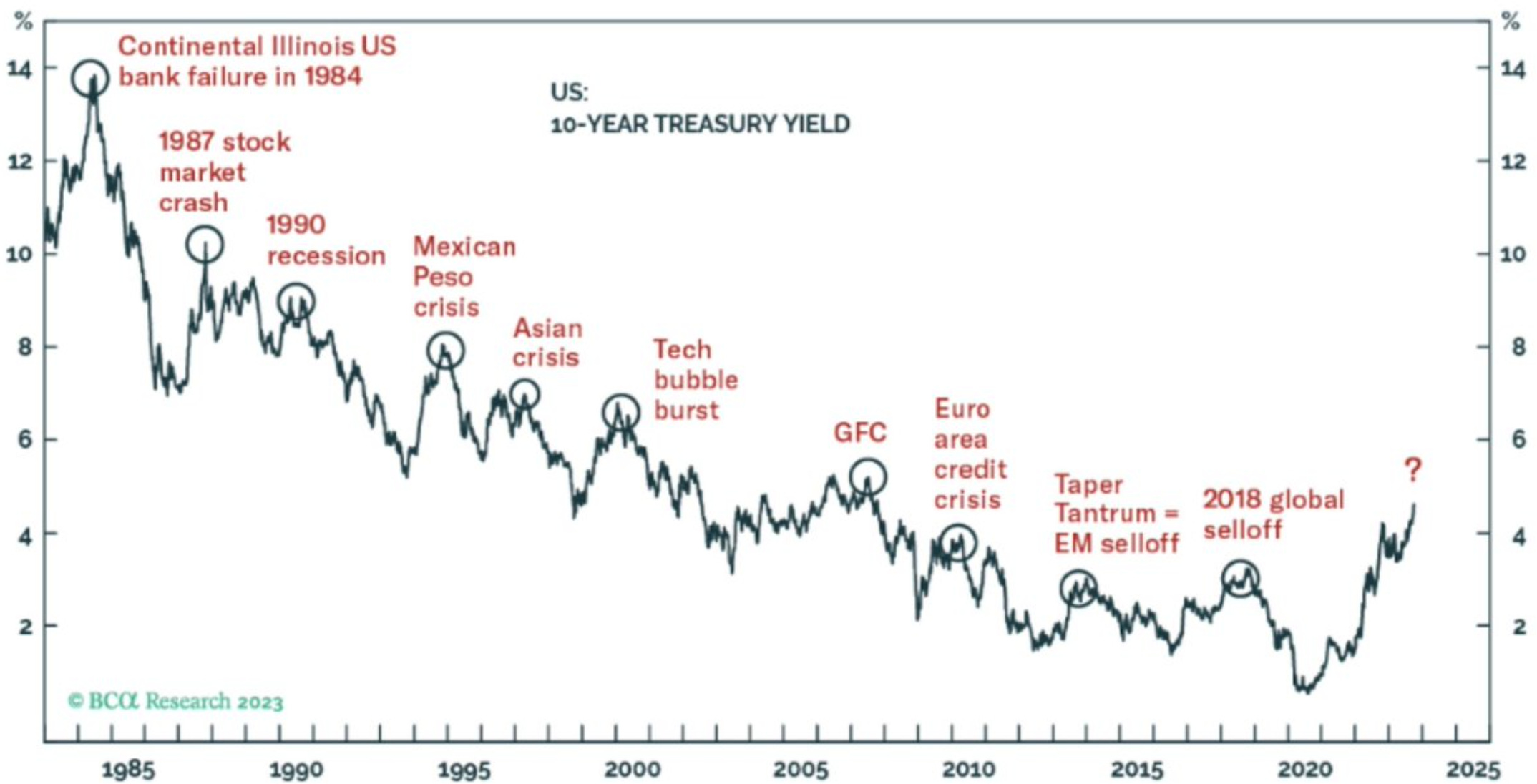

Mortgage rates tend to track the 10-year treasury yield. That moves on the combination of the anticipated Fed actions, what the Fed actually does and how investors react to them.

As the 10-year treasury rises, so do mortgage rates. As it goes down, so do mortgage rates.

Since last week’s Fed meeting, the 10-year has now topped 4.7%. That’s the highest level since October 2007. A 16-year high!

This chart signals one move and that looks higher. If this chart were a stock, you’d be buying it because the chart is screaming that it has momentum and should be moving higher.

As this chart also indicates, throughout history large spikes in the 10-year usually leads to some form of trouble. Something tends to break down. Mortgage rates at 10% could test a lot within the economy, housing market and for consumers.

Now it’s not out of the question that rates tick down. If we’ve learned anything over the last few years, it’s that you can’t rule anything out. What you think may happen, might be wrong. Here are a few scenarios that could cause the easing of rates.

The Fed pivots from their hawkish tone.

High borrowing costs are not helpful to the currently high deficits.

It could become a political issue with the elections upcoming.

As the cost of capital becomes more costly due to high interest rates, it’s harder for businesses and the economy to grow.

Or the higher rates could carry on for longer. With no easing of mortgage rates in sight, they’re clearly headed higher before they head lower. 10% or higher surely looks like a very realistic scenario. Does that cause something to break along the way? Your guess is as good as mine.

The Coffee Table ☕

Joe Wiggins wrote a good piece on short-term thinking when you’re trying to be a long-term investor. Reacting to the day-to-day and things in the short-term skew the long-term focus. The Curse of Short-Termism

After taking a trip to Buffalo with my Dad for the Bills game, this piece by Greg Campion who writes Intentional Wisdom really resonated with me. Why now is the time We always assume there is more time. But we aren’t in control of that. It’s a great post about not waiting and whatever you do, don’t wait.

One of the most universally loved things in this world is coffee. This is a great visual that shows the top coffee producing countries from around the world. I always find it interesting where the coffee I’m drinking originated from.

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.